You helped your son by making the down payment on his new home for him.

You opened a joint account with your daughter so that she may learn about money management while you keep a close eye on her activity.

You loaned money to your brother at a below-market interest rate.

There is nothing to do from a tax reporting perspective, right? Well, no…

First, I would be remiss if I did not mention that there may have been better ways to achieve the specific goals targeted in the above-described scenarios, but the point here is that such scenarios highlight the need to understand gifts and when to file a gift tax return.

You might think you can make gifts to anyone in any amount and not even give a second thought to tax reporting; however, the United States government imposes a limit on the value an individual may transfer without incurring a 40% gift tax, and as of January 1st of this year, that limit (the “exemption”) is $12,920,000. This exemption amount is per donor, not per recipient, and it is for cumulative gifts made during your lifetime. If Congress does not amend the 2017 “Tax Cuts and Jobs Act,” the exemption will be cut to somewhere in the $6-7 million range on December 31st, 2025, so many wealthy individuals are collaborating with their advisors to plan gifts now that consume a majority or all of their exemptions.

In addition, the “freebie gifts,” or gifts that do not consume any of one’s exemption. These include:

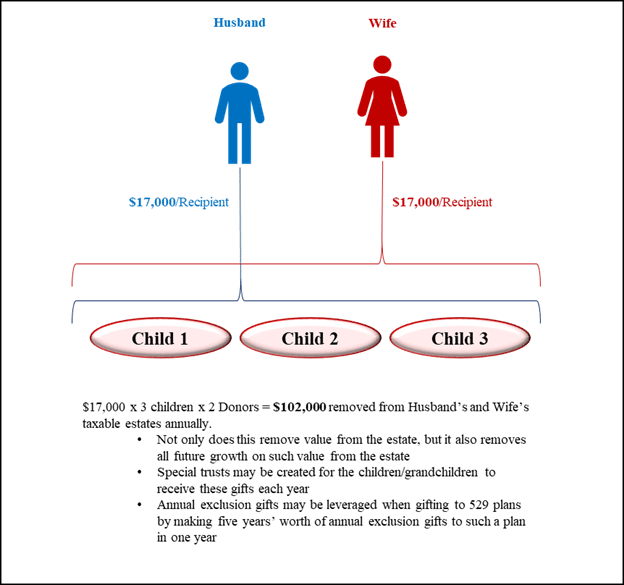

Annual Exclusion Gifts: Everyone is allowed to gift the “annual exclusion” amount (currently $17,000/donor/recipient/year) to as many recipients as s/he would like each year.

Gifts to Political Organizations: The gift tax does not apply to a transfer to a political organization (defined in §527(e)(1)) for the use of the organization.

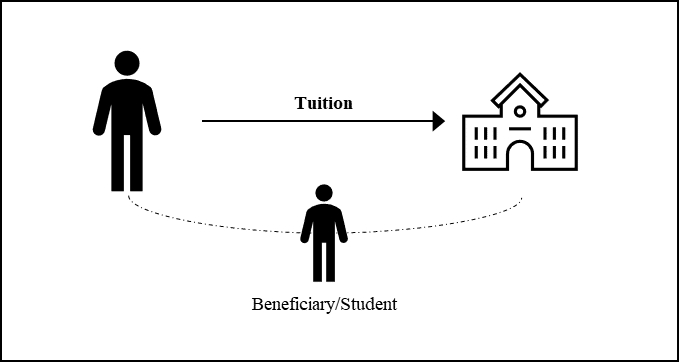

Educational Gifts: Any amounts paid as tuition to an educational organization directly for any individual may be unlimited in value and do not consume one’s gift exemption (I.R.C. 2503(e)(2)(A)).

Gifts to Charities: There is no gift tax applicable to transfers to any civic league or other organizations described in §501(c)(4); any labor, agricultural, or horticultural organization described in §501(c)(5); or any business league or other organization described in §501(c)(6) for the use of such organization, provided that such organization is exempt from tax under §501(a).

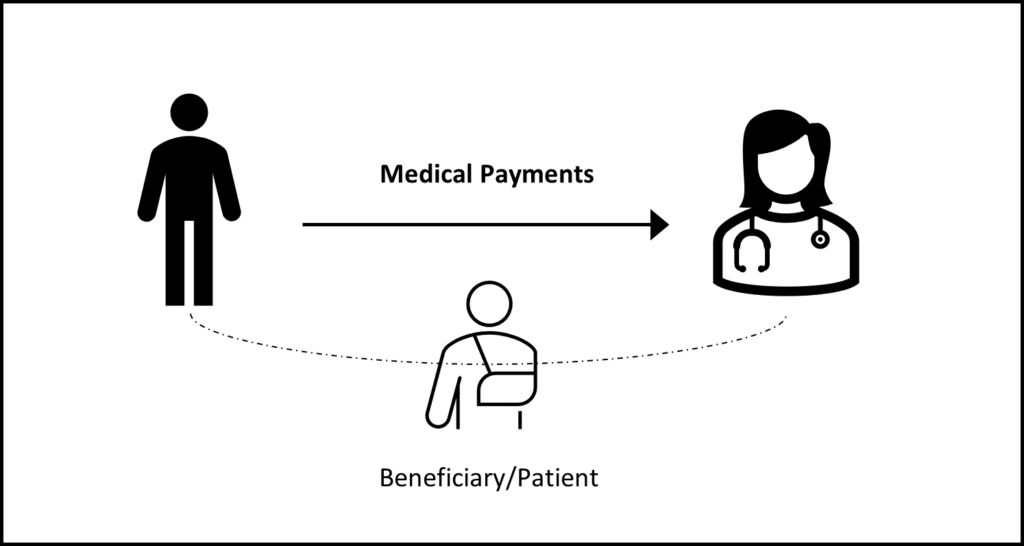

Medical Gifts: Any amounts paid directly to a medical care provider for any individual may be unlimited in value and do not consume your gift or estate tax exemptions (I.R.C. 2503(e)(2)(B)). This includes any expense for which one could claim an income tax deduction for medical expenses, including, but not limited to, preventative care, treatment, surgeries, dental and vision care.

Just because a gift uses your exemption does not mean that you do not have to file a gift tax return (Federal Form 709) for the gift in question. In fact, if you read the instructions for the Federal gift tax return, it is far easier to discern who does not need to file the return than who does. The instructions provide that you are not required to file if you made no gifts during the year to your spouse, you did not give more than [$17,000] to any one recipient, and all the gifts you made were of present interests. We could devote an entire article just to what all of this means; long story short, if you made that down payment for your son, opened that joint account for your daughter, loaned your brother those funds at below-market interest, or transferred real or personal property, whether tangible or intangible to anyone, directly or indirectly, you likely made a gift, and you should consult with your CPA about whether you need to file a Federal (and/or state) gift tax return.

For the freebie gifts, your gift tax return reports that you made such gifts to the Internal Revenue Service, and may address the use of a different, complicated tax for which you have a different exemption: the generation skipping transfer tax. For more substantial gifts, your return reports the gifts and explains how much of your exemption(s) you used to make such gifts. This may require the use of valuations and/or appraisals for gifts of real estate, business interests or other assets that do not have a readily determinable market value. The gift tax return is mostly used to simply report gifts to the IRS without any tax due. If you have used all your exemption(s), you might consider making gifts for which gift tax will be owed with your gift tax return, as there may be substantial benefits for your family if you make such gifts now.

Federal gift tax returns, which may not yet be e-filed, are due when your personal income tax return is due – no later than April 15th of the year after your gift was made (when April 15th falls on a weekend or legal holiday, the due date will occur on the next business day). You may request an automatic six-month extension by filing Form 8892, or if you extend your calendar year Federal income tax return, your gift tax return filing deadline will automatically be extended as well.

If you have any questions or would like to discuss further, please reach out to your client service team, or call 404.264.1400.

Important Disclosures

This article may not be copied, reproduced, or distributed without Homrich Berg’s prior written consent.

All information is as of date above unless otherwise disclosed. The information is provided for informational purposes only and should not be considered a recommendation to purchase or sell any financial instrument, product or service sponsored by Homrich Berg or its affiliates or agents. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. This material may not be suitable for all investors. Neither Homrich Berg, nor any affiliates, make any representation or warranty as to the accuracy or merit of this analysis for individual use. Information contained herein has been obtained from sources believed to be reliable but are not guaranteed. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.

©2023 Homrich Berg.