Now that we are a few months into 2023 with spring break on the mind, many families will inevitably think about what numerous people consider when preparing to board a plane: whether their wills are in good shape. Not only should this question be top of mind, but, as a major tax milestone is now less than two years away, so should the question of how the current federal estate and gift tax laws affect your planning.

Current Federal Gift and Estate Tax Laws

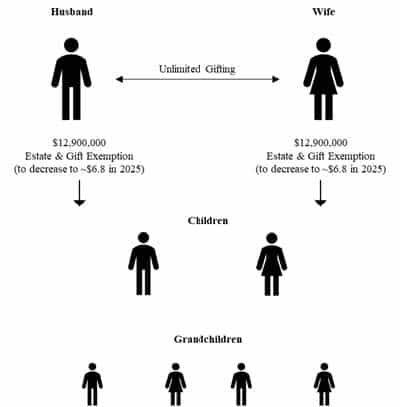

Married United States citizen couples continue to enjoy the ability to gift any amount of value amongst themselves without paying any gift tax. The amount that an individual may transfer to non-spouse beneficiaries (an individual’s “exemption”) is now $12.92 million; total per donor – not per recipient.

This exemption may be used during life for gifts above the annual exclusion (see below for more on this), at death for bequests, or in combination. If you give $2.92 million to your children this year, that leaves $10 million of exemption remaining to make additional gifts or bequests. The exemption will increase slightly in 2024 and 2025 with inflation, and then, if the pertinent schedule established under 2017’s “Tax Cuts and Jobs Act” remains in place, the exemption will effectively be cut in half on December 31, 2025, leaving Americans with an estimated $6.8 million exemption. Currently, for every dollar transferred in excess of one’s exemption to non-spouse recipients, forty cents is paid in the form of gift or estate tax to the United States government (or significantly more if the transfers are to grandchildren and younger generations).

Nearly $13 million, or even $7 million, is very significant, and the estate tax may be no concern of yours. Remember, though, that your “estate” for gift and estate purposes is comprised of all of your assets, including your checking, savings, money market, investment and retirement accounts, the value of your home(s) and other real estate you may own, the death benefit of your life insurance policies, your tangible personal property…everything.

The 2025 decrease to the gift and estate exemptions does not mean that you will owe tax if you give away more than $7 million before 2025, but it does mean that if a $6.8 million exemption will be insufficient to shield your estate from estate taxes at death, now is the time to work with your advisors to explore whether gifting to take advantage of the current laws is right for you, and how.

A Few Gifts to Think About

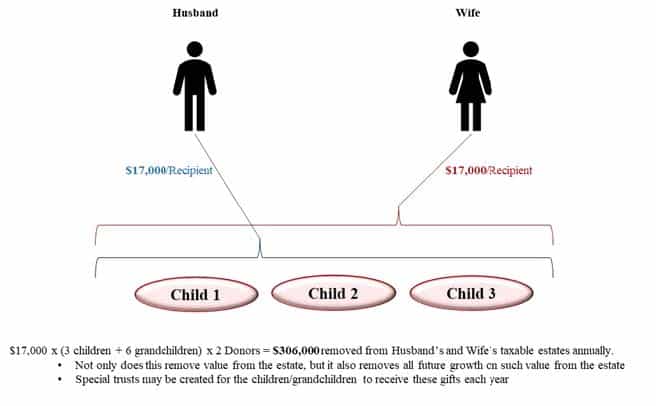

The “annual exclusion” is a freebie in the gifting world. Anyone may give up to the annual exclusion amount ($17,000 in 2023) to an unlimited amount of individuals (or to certain types of trusts benefiting individuals) each year, without consuming his/her gift exemption.

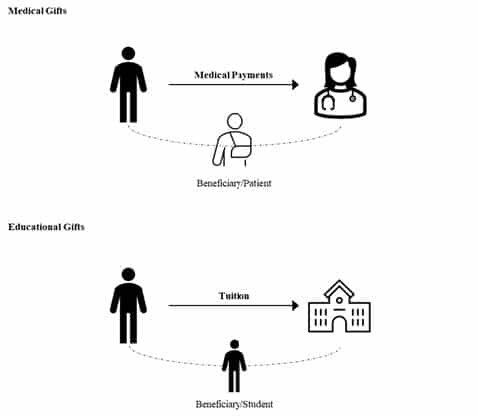

Other “freebie” gifts include medical and educational gifts. Any amounts paid directly to a medical care provider or educational organization for any individual may be unlimited in value and do not consume your gift or estate tax exemptions.

After exhausting the above-explained, applicable gifts, one may want to consider larger gifts to individuals or to irrevocable trusts for the benefit of certain individuals. Trusts allow you to establish rules for who will be in charge of gifted amounts, how those amounts may be administered and distributed, and who may benefit from the gifted assets. They may also allow for the provision of certain additional tax and asset protection benefits for your beneficiaries.

Your wealth advisors should be able to project reasonable growth of your assets and anticipated cash needs, they may help you to determine if you should be gift planning and how much you can afford to gift, and they should work with your attorney and tax account to properly structure gifts in the best way possible to meet both your personal and tax planning needs.

If you have any questions or would like to discuss further, please reach out to your client service team, or call 404.264.1400.

Important Disclosures

This article may not be copied, reproduced, or distributed without Homrich Berg’s prior written consent.

All information is as of date above unless otherwise disclosed. The information is provided for informational purposes only and should not be considered a recommendation to purchase or sell any financial instrument, product or service sponsored by Homrich Berg or its affiliates or agents. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. This material may not be suitable for all investors. Neither Homrich Berg, nor any affiliates, make any representation or warranty as to the accuracy or merit of this analysis for individual use. Information contained herein has been obtained from sources believed to be reliable but are not guaranteed. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.

©2023 Homrich Berg.