Our CIO Stephanie Lang appeared on CNBC‘s Squawk Box yesterday where she discussed the U.S. economy and strong consumers.

Private Security Scams

8/22/2019

The sale of private securities has increased significantly over the last decade. Legitimate private securities may provide increased portfolio diversification and returns. Unfortunately, this has also given rise to fraudulent security schemes. Investors need to be aware, so they do not fall victim to such scams.

Private security offerings do not have to register with the Securities Exchange Commission if they meet minimum guidelines. They are not held to the same scrutiny as public offerings. Advisors and brokers can sell private, unregistered securities to clients with a net worth of at least $1 million or income of $200,000 annually, but agents on the outside of the financial industry are not as well supervised and held to the same standards. It is difficult to identify private security scams because the agents that sell them (insurance agents or former stockbrokers, for example) are not under the supervision of the Financial Industry Regulatory Authority Inc.

Scams go unnoticed until an investor files a complaint with a regulator and an investigation commences.

Additionally, in the past, private securities were sold over the phone or via seminars primarily, but the internet and social media have given scam artists a platform to heavily advertise their investment scams and promises of exciting investment returns to anyone willing to click. They prey upon senior citizens, inexperienced investors, and those without financial advisors. Sadly, these are often people who cannot afford to lose their initial investment.

Unscrupulous registered brokers can also sell fraudulent private securities using a type of transaction called “selling away”. This involves the representative requesting the client to move money from their brokerage account (TD Ameritrade, for example) to their bank account. Then the investment is made from the client’s bank account. This makes it difficult for the broker-dealer firm to supervise.

Here at Homrich Berg, we may alert you to opportunities in private funds occasionally. Those opportunities are reviewed rigorously by our investment department, and we do not receive any commissions on any sales. The investment management fees are the same as if you were invested in a stock, bond, mutual fund, etc. The investment purchase is made directly from your brokerage account. You may hear about private security offerings from your friends. Be sure to run them past your client manager for review before investing.

The sale of private securities will likely continue to grow. Legitimate private securities provide wealthy investors with additional diversification and investment opportunity. Just be aware that not all private security offerings are legitimate.

To find out more, go to https://www.sec.gov/oiea/investor-alerts-bulletins/ia_credentials.html

Homrich Berg Welcomes Evan Byers As Senior Associate

ATLANTA – August 12, 2019- Homrich Berg is pleased to announce the appointment of Evan Byers, CFA, CFP®, CAIA as a new senior associate for the firm. “Evan has extensive wealth management expertise and will be an invaluable asset to HB,” said Andy Berg, co-founder and CEO of Homrich Berg. “ My partners and I are proud to welcome him to HB.”

Evan offers clients more than 8 years of comprehensive wealth management experience, serving as an advisor to high net worth individuals, including multi-generational family offices, corporate executives and entrepreneurs. Evan began his investment career at Fifth Third Bank in Cincinnati, where he managed portfolios for High Net Worth clients, Institutional clients and 401k plans. In addition, Evan maintained research and trading responsibilities for a U.S. Large Cap Equity strategy that was utilized by private wealth clients across the greater Fifth Third footprint. More recently, Evan was an Investment Strategist with SunTrust Private Wealth Management.

Evan holds a bachelor’s degree in Finance and Marketing from the University of Kentucky and a master’s degree from Xavier University. He is also a holder of the Chartered Financial Analyst designation, the Chartered Alternative Investment Analyst designation and has earned the Certified Financial Planner™ designation.

Evan maintains a volunteer position with InheritGA – The Georgia Trust for Historical Preservation and enjoys spending time participating in various financial literacy initiatives sponsored by the ASFIP Foundation. He lives with his wife Paige, and their two dogs in Buckhead.

Disability Insurance

8/9/2019

A disability event can be catastrophic to your financial well-being. Protecting your income should be a top priority. The Council of Disability Awareness states that at least 51 million working Americans are without disability insurance (DI) other than Social Security, which is often inadequate (more on this below).The reality is that a good chunk of us are not prepared for a disability event or even think that we can experience one. However, it’s more common than we may realize. The Social Security Administration estimates that just over one in four of today’s 20-year-olds will become disabled before retirement. This statistic is shocking because over the next decades 25% of us will experience some form of disability. Today, I want to share with you information about the most common types of disability claims, the types of DI, and taxability of DI benefits.

What Are The Common Types Of Disability Claims?

When we think of a disability event, the first thing that comes to mind is a catastrophic accident such as a car wreck that leaves us permanently disabled. Although that could happen to any of us, it’s not that common. Most long-term disability claims are due to musculoskeletal disorders (25%), cancer (15%), pregnancy (9.4%), depression and anxiety (9.1%). A disability event will most likely be an illness and not an accident.

How Do You Protect Yourself From Such Risks?

There are a few ways to protect yourself. The first is Social Security. Although available to most, it’s extremely difficult to qualify under Social Security because its definition of disability is restrictive. The second is group DI. Most employers provide DI as part of your benefits package, and it normally covers 50%-60% of your gross salary. You check a box when you’re electing your benefits, and you’re insured without any medical underwriting. The third option is a personal DI policy. You undergo medical underwriting, and you purchase DI from an insurance company. The individual policy is flexible and can be tailored to your needs.

Are The DI Benefits Taxable?

The taxability of benefits depends on who pays the premium of a disability policy. If your employer pays for the cost of your group DI, then the federal and state government will want a cut of your benefits check. Depending on your tax bracket and the state you live in, the 60% coverage begins to look more like 40-45% of your salary. If you thought it was difficult to live on 60% of your pay, 40-45% is nearly impossible with medical costs being higher and leaving you unable to save. If you’re not saving, then you’re not contributing to your 401(k), and if you’re not contributing to your 401(k), your employer is not matching. I could keep going but you can see how quickly things can turn dire if a disability occurs. Fortunately, you can minimize many of the above risks by purchasing individual DI to supplement your group coverage. Since you’ll be paying the premiums with after-tax dollars, you’ll receive the benefits tax free, and you may even be able to protect retirement contributions. The policy can’t make you whole again, but it can bring you back to 60% of your pay.

Consider doing a review of your current situation. A DI policy can provide you peace of mind that you’ll be okay financially so that you can focus on what matters the most to you.

Andy Berg Named Finalist For National RIA CEO Of The Year Award

ATLANTA –August 8, 2019- Homrich Berg is proud to announce that CEO Andy Berg is one of nine finalists nationwide for the WealthManagement.com Industry Awards in the category RIA CEO of the Year. The ranking celebrates companies, individuals, and organizations that demonstrate outstanding achievement in support of financial advisor success.

Mr. Berg is the co-founder and Chief Executive Officer of Homrich Berg, a fee-only wealth management firm. Andy is currently a member of the Financial Planning Association, the Georgia Planned Giving Council, the Atlanta Estate Planning Council, the Atlanta Police Foundation Board, and the North Atlanta Tax Council.

Andy also serves on the board of directors for the Andrade Faxon Charities for Children, the board of the “I Have A Dream” Foundation, the board of the Atlanta Police Foundation, the Corporate Advisory Board for the Georgia Goal Scholarship Program, Inc., the Atlanta Tipoff Club, the Atlanta Opera, the Buckhead Coalition, and the American Diabetes Association. He graduated cum laude with a BS in Management Accounting from Purdue University.

The winners will be announced at the awards ceremony, which will be held at The Ziegfeld Ballroom in New York City on September 12, 2019.

The Importance Of An Annual Insurance Review

By: Christen Tucker

08/02/2019

Summer is here! Barbecues. Fireworks. Vacations. Makes me think of….a review of homeowners and auto insurance coverage with your insurance agent! Not what you were thinking of? What if you are involved in a car accident on the way to the beach or an out-of-control barbecue chars your home! We hope that doesn’t happen, but are you covered if it did?

Many people view obtaining insurance coverage as a one-time task. Get it and forget it! However, that is not the case. Your old coverage may not suffice especially if you have recently renovated your home or purchased new furnishings, art, or other personal possessions. It is a good idea to make a home inventory and document the items you own. Gather receipts, bills, and brochures to help establish the price and age of everything that would need to be replaced or repaired. Photos and videos of the contents of your home are good documentation tools as well.

When you are ready to review your policy with your insurance agent, be sure to ask the following questions:

Is the coverage on your home and its contents adequate?

The home inventory will help with this. If you have any special items like art, jewelry, or collections (such as stamps or coins), mention them as well. These items may require special coverage.

Is your premium as low as you can expect it to be? Are there any additional discounts available? Can/Should you raise your deductible?

It is a good idea to consider raising your deductibles for losses you can afford to pay.

Are there any losses such as flood or earthquake that may be of concern and are not currently covered in your policy?

Neither flood nor earthquake are covered by standard homeowners policies.

Has anything changed in your coverage from last year?

Insurers may change policy terms at renewal, but they must notify you first. Ask your agent if there are any anticipated changes when the policy renews.

We also recommend that clients secure an umbrella policy to protect them from personal liability. If someone suffers a catastrophic injury on your property or your teenage driver rear-ends a school bus, you can be held liable for lost income, medical bills, and personal damages. While homeowners and auto policies include some coverage, an umbrella policy will protect you from having to sell your home or liquidate your savings if the unthinkable happens. Many insurance agents suggest that your umbrella coverage should roughly equal at least the same dollar amount as your net worth.

These things aren’t the fun part of summer, we know, but life may be a little less hectic this time of year, so it’s a good time to knock off a “need to do” task before you find out too late that your insurance isn’t what you thought.

Please let us know if you have any questions regarding your insurance policies.

4 Tips for Reviewing Your Life Insurance

07/26/2019

Life insurance is an important part of risk management in a financial plan, but it is not a product we typically like to think about. You may have bought a policy in the past and have not looked at it in years. It can be daunting to review your life insurance because there are a lot of moving parts, but here are four aspects to get you started.

1. Amount of Coverage:

Life insurance can have many living benefits, but its primary role should be to provide a benefit in the event of death. Because your needs and circumstances change over time, when reviewing your coverage, it is important to ask the question, “how much do I need and how long do I need it?” You can sit down with your financial advisor or use a life insurance calculator online to determine your need. If you find you have too much or too little coverage, speak with your advisor to help determine your best option.

2. Consider the Type of Policy:

Term Insurance:

Life insurance can generally be grouped into two categories: term and permanent. Term insurance does not accumulate cash value but pays out a death benefit as long as coverage is in force and premiums are paid. If you have term, you do not have to worry about getting an in force illustration on your policy – as long as you pay the premiums then the policy is in force during the term. Employers often offer group term coverage, but keep in mind this is not always portable and can even be more expensive than getting your own individual coverage.

Permanent Insurance:

Permanent insurance policies build cash value over time. Three common types of permanent coverage include universal life (interest rate sensitive), variable universal life (returns based on market performance), and whole life (returns based on dividends paid by the insurance company). Interest rates change, markets fluctuate, and dividend payouts can vary, so it is important to review the policy value periodically.

3. Running an In Force Illustration:

Because universal life insurance cash value returns are based on interest rates, and interest rates are significantly lower than they were 15 years ago, your policy may now be paying a lower current rate. Lower rates on your policy mean it could be underfunded and in danger of lapsing prior to endowment.

You can request an in force illustration to ensure that your policy is adequately funded to meet your goals. This updated illustration will tell you how long the policy will last if you continue to pay the same premium. This illustration can also give you an idea of how much premium is necessary to keep the policy in force until age 100. Knowing this information helps you to evaluate your options and choose what is best for you. You may decide not to change anything, you could continue to own the same policy but change the premium amount paid, or you might look at replacing it with a new policy.

4. Get your Beneficiaries right:

When reviewing your life insurance, you should also make sure your beneficiary designations are done right. Here are a few suggestions:

Keep them up to date – If you have updated your estate plan with trusts or if you have been through a significant life change like a divorce, it is important to ensure that your beneficiaries are up to date.

Not a minor – Do not have your minor child listed as a beneficiary. Instead, set up a trust and make that trust the beneficiary. You can name a trustee to manage the assets for the benefit of the child, which will avoid potential delays and legal issues with getting the funds paid to support them.

Name Contingent Beneficiaries – If your primary beneficiary dies before you (or at the same time), and if no contingent beneficiary is named, the death benefit will then go through the probate process before going to your heirs. Having contingent beneficiaries named will avoid the probate process, potentially saving your heirs from fees and delays in payout.

Long-Term Care Insurance: A Basic Overview

07/19/2019

We are living in a world where health care costs are high and rising while an increasing population of aging adults is living far longer than prior generations. This situation naturally leads to more conversations about long-term care needs for individuals and/or for their aging relatives. Long-term care insurance is designed to offer financial support for medical and non-medical services for people who cannot complete the routine “activities of daily living” (ADLs). ADLs include using the bathroom, bathing, transferring and feeding, dressing, and personal grooming. Qualifications may vary by insurance company and policies, but generally needing assistance for two or more ADLs is the definition used for qualifying for long-term care that might be covered by insurance.

The cost of these services to help a person with their ADLs can create a financial problem for families that may have otherwise thought they were prepared for retirement. For some families facing this potential future financial burden, some form of long-term care insurance may be an effective strategy. Due to the higher likelihood of needing long-term care and the evolving insurance coverage options, it is more important now than ever to review legacy coverage and analyze potential new coverage options.

For years, separate traditional long-term care insurance policies were the industry norm. These policies offered a daily or monthly benefit maximum for a period of years (up to an unlimited amount over a lifetime) with an inflation protection option to cover the rising costs of care. Similarly to health insurance deductibles, such policies would typically have an elimination period (i.e. a waiting period of time before insurance coverage kicks in).

Given the rise in claims linked to people living longer, these policies and the industry landscape have evolved in recent years. The major change affecting legacy policies are large premium increases. Some policies have increased in cost by greater than 50% in one year even though increases typically must be approved by state regulators. Legacy policy holders may either accept the increased annual premium or choose a reduction in benefits to combat the higher premium expenses. The reality of the claims cost situation has led new traditional long-term care policies to become much less affordable for new insurance shoppers while putting a major strain on many existing policies and legacy insurers.

In response to the unaffordable costs of the traditional separate policies, insurance companies have pivoted to hybrid policies that add a layer of long-term care insurance to life insurance products. These policies essentially offer the option for policy owners to choose to use some of their life insurance benefit for long-term care needs instead of a death benefit. As with all insurance, the options and coverages can vary and require careful analysis to determine if they make sense for your family.

As insurance companies react to increasing life spans, rising costs of health care, and a sustained low interest rate environment making it harder for them to grow their balance sheets, we expect to see a rise in hybrid offerings and updates to the second generation of long term care insurance. We encourage families to understand all of their options, including simply building a financial plan to have higher reserves for these costs, before automatically assuming that a long-term care insurance policy is the right way to address their future concerns.

Important Information for College-Bound Children

07/12/2019

This is an exciting time for parents with children headed off to their first year of college. Over the past 18 months or so, you have been planning for this transition, and it may be hard to believe that freshman orientation will be starting soon. Hopefully you have had time to have a meaningful conversation with your son or daughter about what it means to be 18 years old and living away from home for the first time.

In the midst of all the change, many parents and young adults preparing for college may not be aware of how their changing legal status will impact them in a variety of ways. For that reason, we encourage parents who have college-bound children to think about estate planning for their young adults. Estate planning for this age group is easy to overlook, however, having certain documentation in place is highly recommended.

Specifically, we recommend that all parents living in Georgia who have children over the age of 18 should ask their children to sign the Georgia Advance Directive for Health Care form. This statutory form enables a child to name a parent or another trusted individual as a health care agent, and it authorizes health care providers to share medical information with the named agent.

Why this is important: Once children reach the age of majority (which is 18 in Georgia and most other states), they are legally considered adults. As adults, privacy laws generally protect their medical information. We hope you don’t ever need to use it, but in the unfortunate scenario where a child experiences a medical emergency, this document helps avoid any challenges in obtaining information about your child’s medical condition or making decisions on his or her behalf. Additional information, including the form itself and some helpful instructions can be found here: https://aging.georgia.gov/.

Once completed, you should give a copy of this form to people who might need it, such as your health care agent, your family, and your physician. Keep a copy of this completed form at home in a place where it can easily be found if it is needed. Many clients also ask their HB client service team to keep a copy in our files.

If you have children who live in other states, we recommend signing both the Georgia form and the appropriate form for the other state. If you sign more than one form, please be sure to name the same health care agent and backup agent on both. You can find links to forms from other states at this website: https://www.nhpco.org/patients-and-caregivers/advance-care-planning/advance-directives/downloading-your-states-advance-directive/

Homrich Berg Named to 2019 Financial Times 300 Top Registered Investment Advisers

June 27, 2019 – Homrich Berg is pleased to announce it has been named to the 2019 edition of the Financial Times 300 Top Registered Investment Advisers. The list recognizes top independent RIA firms from across the U.S.

This is the sixth annual FT 300 list, produced independently by the Financial Times in collaboration with Ignites Research, a subsidiary of the FT that provides business intelligence on the investment management industry.

RIA firms applied for consideration, having met a minimum set of criteria. Applicants were then graded on six factors: assets under management (AUM); AUM growth rate; years in existence; advanced industry credentials of the firm’s advisers; online accessibility; and compliance records. There are no fees or other considerations required of RIAs that apply for the FT 300. The final list includes advisers from 37 U.S. states.

The final FT 300 represents an impressive cohort of established RIA firms, as the “average” practice in this year’s list has been in existence for over 22 years and manages $4.6 billion in assets. The FT 300 Top RIAs hail from 37 states.

This information reflects Homrich Berg’s views, opinions and analyses as of 07/02/2019 unless otherwise indicated, with no obligation to update. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. The information does not represent legal, tax, accounting or investment advice; recipients should consult their respective advisors regarding such matters. Rankings are not necessarily indicative of future performance.

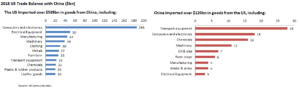

The US China Trade War

By: Ford Donohue

06/21/2019

For months headlines have been dominated by the US China Trade War. As an investor, it’s easy to get caught up in the day to day swings in the market; but we believe that it’s important to take a step back, understand the drivers behind the US-China trade tensions, and make decisions that put portfolios in the best position for long-term growth.

There are two main factors driving the trade war between the US and China: the large bilateral trade deficit and China’s lack of protection for US Tech Intellectual Property (“IP”). As an example of the first factor, the US imports roughly $540bn in goods from China on an annual basis, while China imports just $120bn worth of goods from the US. As an example of the second factor, China often forces US tech companies to divulge proprietary technological information in order to gain access to its market.

The large trade imbalance put consumers at risk when the cost of goods coming from China increase, and the IP transfer issues negatively impact our prized tech sector. Although not everyone agrees on an exact strategy, many politicians and economists agree that imposing tariffs may be an effective way to battle the trade imbalance with China. Due to the large trade deficit, a trade war fought via tariffs is likely to have a much bigger impact on China than it will on the US.

The trade war continues to evolve in real time, and it is difficult to predict where it will go in the weeks and months to come. The US has currently placed 25% tariffs on $200bn worth of goods imported from China and that may increase to cover more imports in the months ahead. However, taking a long-term view, both the US and China have leaders with strong incentives to see their economies grow, not stagnate. As a result, it is unlikely that the trade war continues to escalate significantly from here. At some point, we expect tensions to ease as both leaders will be looking to claim a “victory” in this dispute, although it is impossible to predict exactly when and how.

As investors, it is important to be aware of the facts and understand the impact that the tariffs will have on both economies. We expect the overall impact of this trade dispute on US corporate earnings and GDP to be minimal. Therefore, we believe that investors should stay committed to their long-term plans given the current situation and incentives for both sides.

Social Security Strategy: Restricted Application for Spousal Benefit

By: Jeff Rosengarten

06/14/2019

Are you between the age of 65 ½ and 70? If so, you may be leaving free money on the table from Social Security.

Those who will be age 66 or older by the end of 2019 may be able to claim what is called a “spousal benefit” at age 66 and wait to take their own increased benefit until age 70.

To take advantage of this strategy, you must be over age 66 and your spouse must currently be receiving his or her benefit. If this applies to you file a “restricted application” which allows you to receive one-half of your spouse’s Full Retirement Age (FRA) benefit.

This strategy works best if the lower earner claims their benefit, then the higher earner files a restricted application to receive spousal benefits for a few years and then switches to their own benefit at age 70. In general, we recommend the higher earning spouse delay claiming their own benefit as long as possible to age 70. Each year you delay benefits past age 66, you receive an 8% per year increase in your benefit.

For example, if your spouse is the lower earner and receiving their FRA benefit of $1,000 per month, you would be eligible for a spousal benefit of $500 per month. You could claim the spousal benefit of $500 per month for four years (ages 66 to 70) for a total of $24,000. At age 70, you would switch to your own larger benefit.

Claiming the spousal benefit early at age 66 does not affect your higher benefit so you can keep your increased age 70 benefit intact and still receive some benefits early. The increased benefit will also transfer 100% to your spouse if you pass away first and will continue for your spouse’s lifetime.

If you are divorced and currently unmarried, you can also use this strategy to claim spousal benefits on your ex-spouse’s record at your age 66 and delay taking your own benefit until age 70. You must have been married at least 10 years and divorced for at least two years. Unlike a married couple, your ex-spouse does not have to be currently receiving their own benefit for the spousal benefit to be available, but your ex-spouse must be age 62 or older.

Delaying taking Social Security acts as a hedge against three major risks to your investment portfolio; high inflation, poor markets, and longevity risk (the risk that you outlive your money). Social Security provides Cost of Living Adjustments to keep up with inflation and your benefit does not depend on market performance like the rest of your investment portfolio.

The future of Social Security is largely unknown and out of your control, but deciding how and when to claim your benefit is your choice and will be one of the most important decisions many retirees face. Social Security has no shortage of rules, which means there are plenty of tips and strategies and an equal number of pitfalls. Make sure to do your homework and talk to your advisor to figure out what is best for your situation.

- « Previous Page

- 1

- …

- 16

- 17

- 18

- 19

- 20

- …

- 23

- Next Page »