By: Ross Bramwell

02/27/2019

It appears homeowners have learned from the great recession about not taking on too much debt. However, there is some concern that companies did not learn the same lesson. In the last 10 years since the great recession, companies have been able to borrow significant amounts due to historically low rates. With interest rates low, the economic recovery continuing to extend, and relatively easy lending standards, many companies thought that borrowing for company share buybacks, financing acquisitions, or refinancing old debt was a strategy with little risk. However, over the next few years a significant portion of that debt is maturing which could test that strategy.

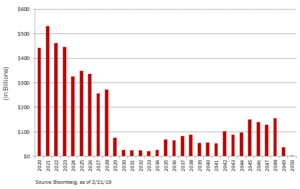

As shown in the below chart, over 50% of the total debt maturing before 2050 matures in the next six years. Although we do not believe current economic conditions indicate a U.S. recession in the short term, this is something to watch as companies may have to refinance this debt as lending conditions tighten or economic conditions potentially worsen. If companies are downgraded due to worsening economic conditions, they would be what investors call “fallen angels,” and that can trigger waves of selling. On the positive side, companies are still making record profits, which allow them to repay their debts, and consumer confidence is still high. We believe one thing is for sure: companies will have to alter their strategies going forward around debt as interest rates have risen and corporate debt levels are already high.

Annual Maturing Debt In Bloomberg Barclays Aggregate Corporate Bond Index

This commentary is for informational purposes only and should not be considered legal, tax, accounting or investment advice. Views and opinions expressed herein are as of the date posted unless indicated otherwise, with no obligation to update. Certain of the information herein has been obtained from third party sources believed to be reliable, but has not been independently verified. Discussions pertaining to potential future events and their impact on the markets are forward-looking in nature, based on current expectations and analysis, and should not be relied upon. Actual results may vary materially.