The SECURE 2.0 Act was signed into law on December 29, 2022 as part of the Consolidated Appropriations Act (H.R. 2617). SECURE 2.0 builds on the Setting Every Community Up for Retirement Enhancement “SECURE” Act of 2019 (H.R.1865) with significantly more provisions. Although there are a number of important provisions in SECURE 2.0, none of them have the impact of the original SECURE Act’s 10-year rule which changed the distribution period for inherited accounts from the beneficiary’s life expectancy to 10 years, except in the case of certain eligible designated beneficiaries. We are still waiting for the IRS to provide final regulations on whether distributions must be prorated or can be deferred until the end of the 10-year period. SECURE 2.0 does nothing to roll-back or clarify the 10-year rule. Despite this, the provisions in SECURE 2.0 are almost all beneficial for taxpayers.

Some of the favorable tax changes in SECURE 2.0 include an increased required minimum distribution (RMD) age, additional ways to fund and access retirement plans, and relief for common retirement plan mistakes. These changes provide a number of tax saving opportunities but to take full advantage of these opportunities will require additional planning. As with any significant legislation, it is important to discuss the changes with your financial advisor to determine how they may impact your personal plan. The number of various provisions in SECURE 2.0 makes categorizing them a challenge, but the most significant provisions impacting individuals tend to fall into one of the following buckets:

- Required Minimum Distributions

- Retirement Plan Contributions

- Accessing Retirement Funds

- Relief for Retirement Plan Mistakes

- 529 and ABLE Plan Enhancements

The planning strategy around RMDs is to try and take the amount of distribution each year that will result in the least overall tax.

Required Minimum Distributions (RMDs)

Increased RMD age. The original SECURE Act increased the RMD age for the first time ever from 70½ to 72. Section 107 of SECURE 2.0 increases the RMD age to 73 for individuals turning 73 during the years 2024-2032. This means that individuals turning 72 in 2023 (and therefore 73 in 2024) will have another year to defer their RMD. Section 107 provides an additional increase in the RMD age to 75 for individuals turning 73 in 2033 or later. Deferring RMDs gives those assets additional time to grow tax-free. However, just because you can defer RMDs doesn’t necessarily mean you should.

The planning strategy around RMDs is to try and take the amount of distribution each year that will result in the least overall tax. Deferring RMDs means you have fewer years over which to spread the distributions. Individuals in a lower tax bracket would likely be better off accelerating distributions to fill up the lower tax brackets. Unfortunately, it is not quite as simple as just filing up the lower brackets. Individuals must also take into consideration the impact a taxable distribution will have on Social Security benefits and Medicare premiums. Individuals can be taxed on up to 85% of their Social Security benefits to the extent their provisional income exceeds $32,000 for married filed jointly ($25,000 single). Similarly, individuals begin paying an income-related monthly adjusted amount (IRMAA) surcharge on their Medicare Part B/D premiums once their modified adjusted gross income exceeds $194,000 for married filed jointly ($97,000 single). For individuals in the highest tax bracket, it may be best to defer RMDs for as long as possible. However, even individuals in the highest tax bracket should consider whether tax rates are expected to rise in the future and whether accelerating distributions or making a Roth conversion could reduce their estate tax liability.

Elimination of RMDs from Roth employer plan. Section 325 of SECURE 2.0 eliminates RMDs for Roth accounts in employer retirement plans beginning in 2024. Currently Roth accounts in an employer plan such as Roth 401(k)s are subject to the RMD rules, while Roth IRAs are not subject to RMDs during the original owner’s lifetime. Upon attaining RMD age, many individuals roll their employer plan Roth account to a Roth IRA so the funds can stay in a Roth account and continue to grow tax-free. SECURE 2.0 appears to eliminate RMDs from all employer plan Roth accounts beginning in 2024, even those accounts from which RMDs are already being taken. Following this change, RMDs will no longer be a factor in the decision to roll an employer plan Roth to a Roth IRA. Instead, the decision should be based on factors such as creditor protection (employer plans generally have more protection), investment options (IRAs generally have more options), and fees (IRAs tend to be less expensive).

A surviving spouse may be treated as deceased spouse for RMDs. Section 327 of SECURE 2.0 provides surviving spouses with a new option regarding a deceased spouse’s retirement account. Beginning in 2024 a surviving spouse may elect to be treated as the deceased spouse. If the deceased spouse is younger, then this would allow the surviving spouse to defer RMDs until the deceased spouse would have reached RMD age. Alternatively, if the surviving spouse is younger then he or she may choose to roll over the deceased spouse’s retirement account into their own account to defer RMDs until the surviving spouse reaches RMD age. Note that a surviving spouse may also simply leave a deceased spouse’s account as an inherited account. This would result in having to take RMDs sooner, but if the surviving spouse has a current need for the funds and the surviving spouse in the case of a rollover (or deceased spouse if electing to be treated as such) is less than 59½ this may be the best option to avoid the 10% early withdrawal penalty.

New Qualified Charitable Distributions (QCD) rules. A QCD is a direct transfer of funds from an IRA to a qualified charity and may be counted toward satisfying all or a portion of an individual’s annual RMD. An individual must be 70½ or older to make a QCD. The maximum annual QCD amount is currently $100,000, but section 307 of SECURE 2.0 provides that this will be indexed for inflation beginning in 2024. QCDs are one of the most tax efficient ways for individuals 70½ or older to make charitable gifts because they can directly reduce up to $100,000 of RMD each year that would have otherwise had to be recognized as taxable income. However, individuals with highly appreciated securities may be better off taking their RMD and offsetting the income by giving the securities (and their built-in gain) to charity. Because charitable giving is such a significant part of income tax planning it is important to speak with your financial advisor to make sure you understand all of your options.

Section 307 of SECURE 2.0 also provides an opportunity to make a one-time QCD election to transfer up to $50,000 to a charitable remainder trust (CRT) or charitable gift annuity (CGA) beginning in 2023. This sounds like a great opportunity to take up to $50,000 of RMD that would have been taxed in the current year and spread it over future years, but there are a number of conditions. First, a CRT/CGA transfer counts toward your annual $100,000 QCD limit and the entire transfer must be completed in a single year. Second, the CRT/CGA must have a minimum annual payout rate of 5% and only the individual making the transfer, or their spouse may receive payments. Third, and perhaps most importantly, all payments are fully taxable at the recipient’s ordinary income tax rate. For CRTs there is an additional requirement that they can be funded only with this one-time QCD. This means the CRT cannot hold assets prior to the QCD transfer or receive additional assets after the transfer. Spouses can each transfer up to $50,000 from their respective IRAs to a single CRT or joint-life CGA for a total of $100,000. Due to the cost and complexity of setting up a CRT, it is hard to imagine anyone setting one up for only $50,000 ($100,000 if both spouses contribute). Because of this a CGA would likely be the best choice for anyone interested in this one-time QCD election.

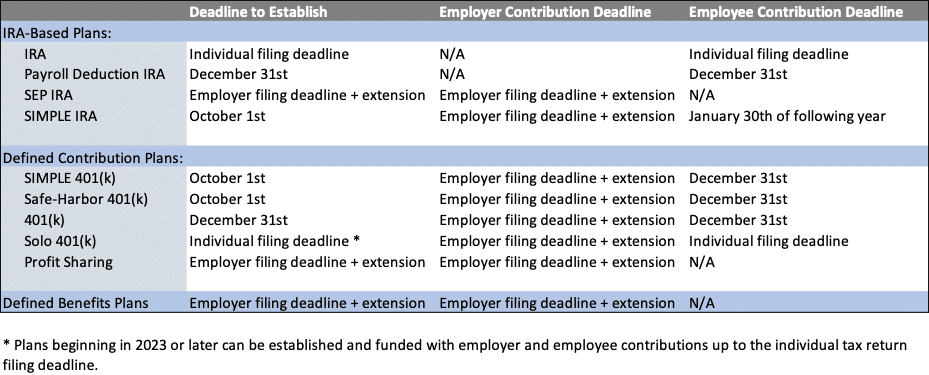

The deadlines for establishing and contributing to retirement plans can also get confusing.

Retirement Contributions

Inflation adjusted IRA catch-up contributions. In 2023 individuals can contribute up to $6,500 to either a Roth or traditional IRA. Individuals aged 50 or older can make an additional $1,000 catch-up contribution. The annual contribution limit is currently indexed for inflation and section 108 of SECURE 2.0 provides that the catch-up contribution limit will be indexed for inflation as well beginning in 2024. Contributions to a traditional IRA are fully deductible unless you or your spouse are covered by an employer retirement plan in which case the deduction is phased out at certain income levels. Contributions to a Roth IRA are not deductible but the funds grow tax-free. The ability to contribute to a Roth IRA is similarly phased out at certain income levels.

Solo-401(k) deadline extended. Currently SEP IRA accounts and certain other employer plans can be established and funded after year-end, up to the employer’s tax filing deadline plus extensions. Section 317 of SECURE 2.0 now allows one-participant 401(k) plans (with plan years beginning in 2023 or later) to be established and funded after year-end, up to the individual tax filing deadline. These plans are also known as solo-401(k) plans and are only available to businesses owners who have no full-time employees (except for their spouse). There has been some uncertainty as to whether one-participant 401(k) plans could be established after year-end and it appears these plans can still be funded with the employer contribution up to the employer’s tax filing deadline plus extensions, but Section 317 makes it clear that with regard to employee contributions the plan must be established and funded by the individual filing deadline. For example, a business owner can now wait until April 1, 2024, to establish and make 2023 contributions to a one-participant 401(k).

The employer and employee designations can be confusing. Self-employed business owners are essentially both the employer and employee. However, there can be a distinction for purposes of retirement contributions. A business owner with a one-participant 401(k) may elect to defer (i.e., contribute as an employee) up to $22,500 of their compensation in 2023 ($30,000 if age 50 or over). The business can then contribute (as the employer) up to 25% of the business owner’s compensation, provided the total employee and employer contributions cannot exceed $66,000 for 2023 ($73,500 if age 50 or over). For single owner businesses earning over $300,000 per year the employee vs. employer contribution distinction doesn’t really matter because the maximum contribution could all come from the business (i.e., the employer) since 25% of $300,000 exceeds the $66,000 contribution limit. However, the distinction can be important for single owner businesses making less than this. For example, if a business were to earn $100,000 in 2023 then the business (i.e., the employer) could only contribute $25,000 (25% of $100,000), but the business owner (i.e., employee) could contribute an additional $22,500 ($30,000 if age 50 or over). This is where the deadlines for establishing and contributing to a plan become important and why the ability to establish and contribute to a one-participant 401(k) as late as the individual filing deadline can make a difference for certain business owners.

The deadlines for establishing and contributing to retirement plans can also get confusing. The chart below lists the deadlines for most plans. Note that the dates in this chart are for the plan year unless otherwise noted (i.e., a SIMPLE IRA for 2023 must be set up by October 31st of 2023), while the filing deadlines are for the year following the plan year (i.e., you have until April 2024 to file your 2023 tax return and you have until April 2024 to setup and fund a Solo 401(k)).

Increased employer plan catch-up contributions. Beginning in 2025, section 109 of SECURE 2.0 increases employer retirement plan (e.g., 401(k) and 403(b) plan) catch-up contribution limits for individuals ages 60-63 to the greater of $10,000 or 150% of the standard catch-up limit currently in place for those age 50 or over ($7,500 in 2023)). Note that Congress only increased the catch-up limit for individuals ages 60-63 and it drops back to the standard catch-up limit for those age 64 or over. In addition, section 603 of SECURE 2.0 states that beginning in 2024, catch-up contributions made by employees with wages in excess of $145,000 must be designated Roth contributions. This applies to all employer plan catch-up contributions, not just the increased catch-up contributions for individuals ages 60-63. Note that employer retirement plans are not required to accept Roth contributions. However, Section 603 essentially disallows all catch-up contributions if the plan does not allow Roth designated catch-up contributions. This provision will likely cause many employers to modify their retirement plans to allow Roth contributions if they do not do so already.

Increased SIMPLE plan catch-up contributions. Beginning in 2025, section 109 of SECURE 2.0 also increases SIMPLE IRA and SIMPLE 401(k) catch-up contribution limits for individuals ages 60-63 to the greater of $5,000 or 150% of the standard catch-up limit currently in place for those age 50 or over ($3,500 in 2023). SIMPLE IRA and SIMPLE 401(k) plans are only available to an employer with 100 or fewer employees, and the employer is required to either match employee contributions on up to 3% of compensation or make a contribution for each eligible employee in an amount equal to 2% of their compensation. Note that the Roth requirement for catch-up contributions mentioned above does not apply to SIMPLE plan or IRA catch-up contributions which can continue to be made pre-tax.

Roth designated employer match. Beginning in 2023, section 604 of SECURE 2.0 allows defined contribution plans to give participants the option of receiving matching contributions on a Roth basis. This means that all contributions to a Roth 401(k) plan can now be after-tax contributions, not just the employee portion. However, section 604 also provides that any Roth designated employer contributions will be included in the employee’s income. For example, if an employer plan provides up to 3% matching contributions, then an employee that earns $100,000 and contributes $3,000 to their Roth 401(k) could elect to have the $3,000 employer match also be a Roth contribution, but this would increase the employee’s income for tax purposes by $3,000. Individuals who anticipate paying taxes at a higher rate in the future should consider contributing to a Roth 401(k) and having any employer match be made on a Roth basis as well if possible. Note that although employers are currently allowed to make Roth designated contributions, it will take some time for employers and plan administrators to get this implemented.

Student loan payments qualify for matching contributions. Beginning in 2024, section 110 of SECURE 2.0 allows an employee’s student loan payments to be treated as retirement plan contributions for purposes of the employer match. This is a great benefit for anyone with student loans who may not have the funds to contribute to their retirement plan in addition to making their student loan payments. This benefit is likely to become something younger candidates look for in an employer.

SECURE 2.0 not only creates additional retirement contribution options and incentives, but also provides a number of new ways that individuals can access their retirement funds without penalty.

Accessing Retirement Funds

SECURE 2.0 not only creates additional retirement contribution options and incentives, but also provides a number of new ways that individuals can access their retirement funds without penalty. Distributions from retirement plans other than Roth plans are subject to ordinary income tax, and distributions taken before age 59½ are subject to an additional 10% early withdrawal penalty unless an exception applies. Below are some of the exceptions to the 10% early withdrawal penalty currently available:

- Disability: Withdrawals after the plan participant/owner becomes disabled.

- Military Service: Withdrawals by certain qualified military reservists during active duty.

- Medical Expenses: Withdrawals for unreimbursed medical expenses that exceed 10% of adjusted gross income.

- Insurance: Withdrawals to pay certain health insurance premiums while unemployed (limited to IRA plans).

- Education: Withdrawal is for certain qualified higher education expenses (limited to IRA plans).

- Home Purchase: Withdrawals of up to $10,000 for qualified first-time homebuyers (limited to IRA plans).

- Birth or Adoption: Withdrawals of up to $5,000 for birth or adoption related expenses.

- Equal Payments: Withdrawals taken as a series of substantially equal payments that are calculated based on life expectancy and meet certain requirements.

- Separation from Service: Withdrawals by employees who separate from service (i.e., leave their employer) at age 55 or older (age 50 or older for public safety employees).

SECURE 2.0 expanded the list of 10% early withdrawal penalty exceptions to include the following:

- Equal Payments (expanded): Beginning in 2024, the equal payment exception is expanded to allow individuals to make partial rollovers or transfers of accounts from which exempt equal payments are currently being made, provided the total distributions from the original and rollover accounts are equal to the distributions that would have been taken from the original account. It does not appear that the distributions from the original and rollover accounts have to be in proportion to their balances as long as the total distributions equal the original distribution amount. This change could be significant for individuals who have been taking equal payments to qualify for the exception. Prior to this rule going into effect (in 2024), rollovers or transfers trigger a retroactive 10% early withdrawal penalty on all distributions taken before age 59½ pursuant to the equal payments exception.

- Separation from Service (expanded): Beginning in 2023, the exception for employees who leave their employer is expanded to include corrections officers, forensic security employees, and employees providing firefighting services that are age 50 or older as well as public safety employees with at least 25 years of service under the plan (the legislation is unclear as to whether the 25 years of service have to be with the same employer).

- Terminal Illness: Beginning in 2023, there is an exception for distributions to a terminally ill individual, which for purposes of this exception is an individual who has been certified by a physician as having a condition which can reasonably be expected to result in death in 84 months (significantly more than the standard definition’s 24-month timeframe).

- Federal Disaster: Individuals with their principal abode located within a Federally declared disaster area may withdraw up to $22,000. This exception is retroactive back to 2021 but going forward the withdrawal must generally be taken within 180 days of the disaster. Income tax resulting from the withdrawal may be spread evenly over the three-year period that begins with the year of distribution and withdrawals may be repaid within three years to avoid paying tax on the distribution. In addition, individuals with their principal abode located in a Federally declared disaster area may take a loan from their qualified plans of up to 100% of their vested balance or $100,000 and they have an additional year to repay the loan if taken within 180 days of the disaster (the repayment period is generally five years).

- Emergencies: Beginning in 2024, individuals may withdraw up to $1,000 during a calendar year for unforeseen or immediate financial needs relating to necessary personal or family emergency expenses. Subsequent emergency withdrawals are not allowed until the prior withdrawals have been repaid, the individual makes contributions to the plan equal to the withdrawal amount, or three years have passed since the withdrawal. Beginning in 2024, employers will also be able to establish Roth designated emergency savings accounts linked to existing employer retirement accounts and eligible for matching contributions. However, these emergency savings accounts are only available for employees earning less than $135,000 per year and contributions must cease when the account reaches a maximum of $2,500.

- Domestic Abuse: Beginning in 2024, victims of domestic abuse may withdraw up to the lesser of $10,000 or 50% of their vested balance from most defined contribution plans. Withdrawals must be taken within one year of the abuse and may be repaid within three years to avoid tax on the distribution.

- Long-Term Care: Beginning in 2026, withdrawals of up to $2,500 per year will be allowed to pay long-term care insurance premiums. The other early withdrawal penalty exceptions under SECURE 2.0 are geared toward emergencies, but the long-term care insurance exception gives individuals an additional planning option around a potential future benefit. It is important that you discuss long-term care options with your financial advisor to determine if the use of retirement funds to pay for long-term care insurance is the best use of those funds.

Note that the exceptions mentioned above may allow you to avoid the 10% early withdrawal penalty, but you will still have to pay income tax on the amount distributed unless it is repaid. It is best to leave funds in retirement accounts to the extent possible so they can continue to grow tax deferred. As mentioned above, individuals turning 73 in 2024 or later can defer their RMDs until at least age 73.

Essentially, if you catch the mistake within two years then you get the penalty reduction, but if the IRS catches the mistake, then you are out of luck.

Relief for Retirement Plan Mistakes

SECURE 2.0 contains a number of provisions providing relief from retirement plan mistakes. Historically the penalty for failing to take an RMD has been significant (50% of the RMD amount that was not distributed). Beginning in 2023, section 302 of SECURE 2.0 reduces the penalty for failing to take an RMD from 50% to 25%. The penalty can be further reduced to 10% if the RMD is taken during the “correction window” which ends upon the earliest of the following: 1) notice of deficiency is sent, 2) tax is assessed, or 3) the last day of the second tax year after the tax is imposed (i.e., becomes due). So, to qualify for the penalty reduction for an RMD that was failed to be taken in 2023 could be taken as late as December 31, 2025, but should be taken as soon as possible to avoid missing the correction window as a result of a notice of deficiency or tax assessment. Essentially, if you catch the mistake within two years then you get the penalty reduction, but if the IRS catches the mistake, then you are out of luck.

Section 305 of SECURE 2.0 is not a legislative change, but rather directs the IRS to make changes to the Employer Plans Compliance Resolutions System (EPCRS) by the end of 2025. EPCRS is laid out in IRS Revenue Procedure 2021-30 and permits self-correction of inadvertent failures to comply with employer retirement plans (e.g., 401(k) and 403(b) plans). SECURE 2.0 provides for more types of plan errors to be self-corrected, specifically allowing for self-correction of errors relating to loans to the plan participant. However, a more significant change may be the expansion of EPCRS to permit self-correction of IRA errors. SECURE 2.0 specifically expands EPCRS to allow for waivers of the penalty for missed RMDs and for non-spouse beneficiaries of inherited IRAs to return distributions that they inadvertently took, not realizing it would be treated as income. In addition, SECURE 2.0 directs that the correction period under EPCRS be indefinite provided corrective action has begun prior to the error being discovered by the IRS. So, as with the missed RMD penalty discussed above, it is important to address mistakes as soon as possible to have the penalties waived.

Section 313 of SECURE 2.0 provides that the statute of limitations for penalties relating to an RMD shortfall (i.e., missed RMD) or excess IRA contribution begins when the individual income tax return (Form 1040) is filed for the applicable tax year (or as of the tax filing deadline if no income tax return is required). Previously the statute of limitations for these penalties did not begin until Form 5329 (where these penalties are reported) was filed. However, if you did not know there was a mistake then you would not know to file Form 5329, so the statute of limitations often remained open indefinitely. The statute of limitations for assessing a penalty on an RMD shortfall is three years while the statute of limitations for assessing a penalty on an excess IRA contribution is six years. As mentioned above, beginning in 2023 the penalty for failing to take an RMD is 25% of the undistributed amount, with a chance to reduce the penalty to 10%. Excess IRA contributions are taxed at 6% per year for each year the excess amounts remain in the IRA.

Although you can have only one designated beneficiary of a 529 plan at any time, it is a simple process to change the designated beneficiary.

529 and ABLE Plan Enhancements

529 rollover to Roth IRA: One of the most talked about provisions in SECURE 2.0 is the ability to rollover funds from a 529 plan to a Roth IRA beginning in 2024. Section 126 of SECURE 2.0 states that 529 plan distributions will not be subject to income tax or penalty if they are made directly to a Roth IRA for the benefit of the designated beneficiary of the 529 plan subject to the following conditions:

- The 529 plan of the designated beneficiary has been maintained for at least 15 years;

- Only 529 plan contributions (and earnings on those contributions) made at least five years prior to the Roth IRA transfer are eligible;

- The amount transferred during any year cannot exceed the annual Roth IRA contribution limit which for 2023 is the lesser of the beneficiary’s taxable earnings or $6,500 ($7,500 if age 50 or older) reduced by any other IRA contributions during the year; and

- The maximum amount transferred for a beneficiary cannot exceed $35,000 during their lifetime.

One thing to note is that while generally only individuals who fall below a certain income threshold may contribute to a Roth IRA, the income limitation does not apply to these qualifying 529 distributions.

Unfortunately, the legislation is not clear regarding how changing the designated beneficiary of a 529 plan would impact the eligibility and timeframe of a Roth transfer. Ideally, if a 529 plan had funds not needed for education expenses, the owner of the plan could change the designated beneficiary to themselves or their spouse and transfer the funds to a Roth IRA for their benefit. They could then change the designated beneficiary to another qualified family member and transfer funds to a Roth IRA for their benefit as well.

Although you can have only one designated beneficiary of a 529 plan at any time, it is a simple process to change the designated beneficiary. In fact it is fairly common for a family to have only one 529 plan for multiple children. After the first child finishes college, the plan owner simply changes the designated beneficiary to the next child attending college. However, if changing the designated beneficiary restarts the 15 year period the plan must have been maintained to qualify for the Roth IRA rollover then families may need separate 529 plans for each child (and possibly for the parents as well).

It appears that the intent of this legislation is to encourage 529 plan contributions by helping to alleviate the concern that there will be remaining funds that can only be accesses through a non-qualified withdrawal (subject to income tax and a 10% penalty). Hopefully Congress or the IRS will provide guidance soon that provides flexibility with regard to beneficiary changes.

ABLE age limit increased: Section 126 of SECURE 2.0 increases the age by which an individual must become disabled to be eligible for an ABLE account to 46, beginning in 2026. An ABLE (529A) account is tax-advantaged savings accounts for individuals with disabilities. The annual contribution to an ABLE account is $17,000 in 2023 and the total contribution limit is subject to each state’s limit for education-related 529 accounts. In addition to being tax-advantaged, ABLE accounts generally do not impact an individual’s eligibility for SSI, Medicaid, and means-tested programs. Currently, ABLE account eligibility is limited to individuals who became disabled before turning 26 years of age, but you can establish an ABLE account after age 26 as long as you became disabled before your 26th birthday. Similarly, it appears that individuals will not have to be under age 46 in 2026 (the effective date of this legislation), but simply have been under age 46 at the time they became disabled. This should allow significantly more disabled individuals to be eligible for ABLE accounts.

Summary

This piece covers the more significant SECURE 2.0 provisions impacting individuals, but SECURE 2.0 is an enormous piece of legislation and there are other provisions that will be important to specific individuals. As with any significant legislation, it is important to discuss the changes with your financial advisor to determine how they may impact your personal plan.

Important Disclosures

This article may not be copied, reproduced, or distributed without Homrich Berg’s prior written consent.

All information is as of date above unless otherwise disclosed. The information is provided for informational purposes only and should not be considered a recommendation to purchase or sell any financial instrument, product or service sponsored by Homrich Berg or its affiliates or agents. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. This material may not be suitable for all investors. Neither Homrich Berg, nor any affiliates, make any representation or warranty as to the accuracy or merit of this analysis for individual use. Information contained herein has been obtained from sources believed to be reliable but are not guaranteed. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.

©2023 Homrich Berg.

Resources:

https://www.congress.gov/bill/116th-congress/house-bill/1865

https://www.congress.gov/bill/117th-congress/house-bill/2617/text

https://www.ssa.gov/benefits/retirement/planner/taxes.html

https://www.irs.gov/publications/p560

https://www.irs.gov/pub/irs-drop/rp-21-30.pdf

https://www.irs.gov/pub/irs-pdf/p970.pdf

If you have any questions or would like to discuss further, please reach out to your client service team or call 404.264.1400.