")

04/26/20

We hope our communication this week continues to find you healthy and enjoying quality time with your family. It is hard to believe that it has been six weeks since most of the country entered into this shelter-in-place environment and we all look forward to a gradual return to some level of normalcy over the coming weeks and months. Currently, there is a wide dispersion of opinions in the media on the recovery of the economy and we thought we’d provide you our perspective in this commentary.

Over longer time periods, stocks tend to follow the path of corporate earnings. However, in the short term, they can be driven by a number of factors. These daily, weekly, and monthly moves are heavily influenced by investor expectations. The stock market’s value today is a reflection of, and is pricing in, future expectations, whether positive or negative. We believe short-term moves are often then a consequence of a change in expectations as investors receive more information. For example, if a public company is expected to have a 5% loss in earnings but reports only a 2% loss, the company’s stock will likely increase in value because it beat expectations. The same is true for a company that reports positive earnings of 5%, but comes in below expectations of 7%, its stock price will likely decline in value even though it had positive earnings. The move was determined by what was previously priced into its value already — the expectations.

We’ve seen how expectations have impacted financial markets in the last few weeks. The stock market was near its recent lows in late March when coronavirus deaths dominated the news and the forecasts were dire regarding how far we might be from a peak. Modeling was showing a wide range of scenarios from 100,000 to over 200,000 U.S. deaths. However, in early April updated modeling accounting for the social distancing measures enacted began to show expected U.S. deaths to be significantly lower than first thought, in the range of 60,000-70,000 deaths, and hot spot states such as New York also began to see some improvement. Even the lower projections would have seemed unthinkable to many in January, but given that 60,000 is significantly lower than 200,000 possible deaths, it was a positive change in the outlook. During these same few weeks, the U.S. economy lost over 22 million jobs while the S&P 500 rebounded over 30% at one point off its lows. It’s hard to rationalize how those two could occur at the same time, but it appears the unprecedented job losses were priced in early as the shelter-in-place mandates were enacted.

This week, another important economic indicator will be reported: first quarter’s U.S. GDP growth. This measure is the percentage change in gross domestic product from the previous quarter, annualized. Given the lockdowns were enacted unevenly across the U.S., it’s been hard to estimate how bad this number could be. It is very likely that we could see a large negative number this week, but it may not be quite as bad as it appears. For example, it may be reported that U.S. GDP declined as much as 30%. That does not mean GDP dropped 30% from the fourth quarter. The 30% drop indicates that GDP declined 7.5% from the prior quarter, but that number is then multiplied by four to be annualized which can make for a misleading headline. Current expectations are for a number lower than -30% annualized, but remember no matter what number is announced that it has been annualized.

Looking forward, it is very likely that second quarter GDP reported at the end of July will be even worse, and that the third quarter and fourth quarters will surely be impacted as well. However, it’s likely we will be in some form of a recovery in the second half of this year. We know parts of the economy have been completely shut down and many sectors will continue to be for many months ahead. As we discussed in our last investment email, a ‘V’ recovery is unlikely for jobs or GDP. During the 2008 recession, GDP declined for a total peak-to-trough drop of 4%. Over the course of the Great Depression, by contrast, GDP fell 26%.

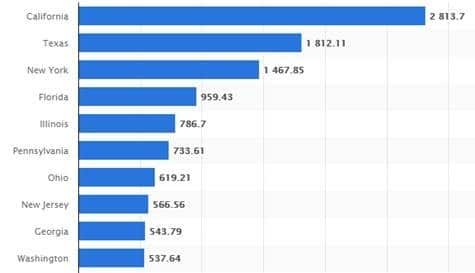

Although the GDP number next week may not be as scary as it first appears, the level of unemployment, the need for more stimulus, and the other economic realities still lead us to believe that the recovery will be quite gradual. Georgia made national headlines this week by beginning to lift restrictions. There are other individual states and groups of states working together that are looking at how to open their economies over the coming weeks. However, for many states reopening is not likely to happen soon. California, which is the fifth largest economy in the world, ranking ahead of India and behind Germany, and New York, the U.S.’s third largest economy, are both not looking at reopening anytime soon. California and New York alone make up about 23% of U.S. GDP. In addition, as the world continues to be locked down the demand for oil has plummeted which has left many oil-related companies facing substantial job losses and even bankruptcy. The entire energy sector is suffering which will should have a prolonged impact on energy-dependent Texas, which is the second largest economy in the U.S.

Ten Largest States by GDP for Q4 2019 (data in millions)

Source: Statista 2020

Just this past week on national television, a small business owner from Decatur was explaining the issues she faced in reopening her business. Requirements for sanitation and use of personal protection equipment (PPE) will not be easily met in the current environment. Select businesses may be able to continue to take advantage of online sales, delivery options, and reopen store fronts quicker. However, many parts of the economy may be more like a turtle’s head coming out of its shell slowly and tentatively, and probably a little jumpy. We imagine many of us, as consumers, will be that way too. Ultimately, widespread testing and viable medical options including a vaccine and/or effective treatments will be needed for the economy to fully open. The government passed another stimulus bill this week to help more small businesses, but additional aid may be needed to support local and state governments as their budgets are hit by lower tax revenues due to the shutdowns.

We certainly hope for the best as we begin to reopen and move towards a recovery, but we acknowledge that we are still dealing with many unknowns. The stock market has rebounded more than expected, and we believe it is currently expecting, or pricing in, a pretty rosy scenario this summer. The risk is if those rosy expectations are not fully met, the stock market may wither back to a reality where the recovery will be a little more gradual and a little tougher. As we expect it won’t be a smooth ride until the recovery is well entrenched, we continue to stay firm believers that a maintaining a diversified approach, staying within your desired level of risk, and looking for opportunities that present themselves during this challenging time are the best approach. As always, we hope you and your family stay safe and well over the coming months. If you have any questions, please reach out to a member of your client service team.

Disclosures: The information reflects Homrich Berg’s views, opinions and analyses as of April 26, 2020. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. The information does not represent legal, tax, accounting or investment advice; recipients should consult their respective advisors regarding such matters. Certain of the information herein is based on third party sources believed to be reliable but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.