By: Todd Hall and Andy Bunch

11/18/2020

The rest of 2020, and likely most or all of 2021, could prove to be an important period of estate planning for your family. Transferring assets to the next generation typically plays an important role in an estate plan and potential changes in the coming months could change the allowable transfer amounts or other features of current estate laws.

Current gift tax laws allow an individual to give up to $15,000 per year per recipient. Once gifts to any individual recipient go above that amount in a given year, the excess utilizes some of your lifetime exemption. The estate tax lifetime exemption is the amount you can transfer to the next generation without incurring gift or estate tax. You can use some or all of this exemption during life, and any amount not used will be available at death, depending on the laws at the time of death. Any amount in excess of the exemption is taxed at 40% under current law.

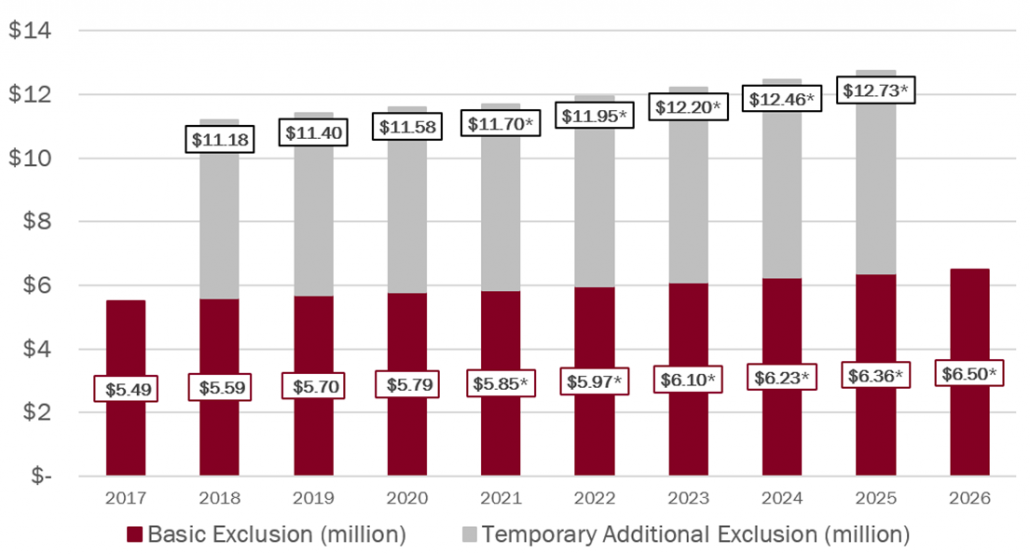

Unique Opportunities in Current Law: The Tax Cuts and Jobs Act (TCJA) temporarily doubles the Estate & Gift Tax Exemption (as set out by the American Taxpayer Relief Act of 2012) through the end of 2025. At that point, the law is scheduled to “Sunset” and revert back to the lower limit (indexed for inflation). In 2020, the exemption is $11.58 million per person, or $23.16 million per couple, and one could think of this amount as two parts: a basic exclusion increasing with inflation each year, and a temporary additional exclusion that is scheduled to vanish in 2026 under the current tax law.

* Amounts shown for 2021 are estimated based on 2020 available data. Amounts for years 2022 through 2026 assume a 2.13% inflation adjustment each year. Actual inflation may be different. This information is current as of 10/2020. Homrich Berg does not provide tax, accounting or legal advice, and information presented about tax considerations is for informational purposes only and not intended as tax advice. Please consult your legal or tax advisor(s).

What Could Change Next Year: Current news reports indicate that Republicans will have 50 seats in the Senate, and Democrats have 48. Both of Georgia’s Senate seats will be decided by a runoff election on January 5. If Republicans win either or both of these seats, they will retain control of the Senate. If Democrats win both seats, both parties will be tied with 50 Senators and control of the legislative calendar will likely change to the Democrats, assuming Joe Biden ultimately wins the Presidential election. This means we will either have divided government in 2021, or Democrats will have control but with no wiggle room to lose any Senate votes on legislation. Legislation is always unpredictable, and so are effective dates for any changes. Even if tax changes are passed into law during 2021, they might not apply until 2022, leaving time for additional estate planning next year.

Taking Advantage of Current Law: Families with a net worth of greater than $13 million for a married couple (or $6.5 million if single) may have an estate tax if they live to 2026 or later, and laws remain unchanged. Every additional $1.00 of growth above that level could result in another $0.40 of taxes at death. Families in this situation should talk to their advisor about whether it is advisable to make significant gifts in trust while the exemption is temporarily at the higher level.

In 2020, each individual can give $11.58 million to the next generation without gift or estate tax. If someone with a large estate were to make a gift of this amount into a trust for future generations, and current law remains unchanged, this would result estate tax savings of over $2 million* at death, and possibly significantly more depending on how much assets grow after a gift is made.

For a married couple, one spouse could give up to $11.58 million to the other spouse in a special kind of trust called a Spousal Lifetime Access Trust (SLAT). This could result in significant estate tax savings and the ability of the beneficiary spouse to access the funds for life if needed.

It is important to work with an attorney who is an expert in the field of estate and trust law when implementing planning like this. It is also important to review with your financial advisor how much can or should be gifted to trust, and which assets are best to use. With that said, there are significant opportunities in current law that are currently scheduled to go away on January 1, 2026, and may go away sooner if Congress takes action before then.

For those with a net worth of more than $13 million for a married couple, or $6.5 million for a single person, we believe it is appropriate to discuss whether or not these or other strategies may be appropriate in your specific situation.

* Tax savings of $2 million are based on the assumption that a family removes $11.58 million from the taxable estate and current law remains unchanged. Assuming death occurs in 2026 when the exemption is projected to be $6.5 million, the difference between the $6.5 million exemption and the $11.58 million of gifts made in 2020 is $5,080,000. If left in the taxable estate and taxed at 40%, these assets would generate $2,032,000 in estate taxes at death in 2026.