Homrich Berg is pleased to announce it has been named to the 2020 InvestmentNews Best Places to Work for Financial Advisers. The third annual InvestmentNews Best Places to Work for Financial Advisers highlights 75 firms that recognize the importance of a strong workplace culture and stand as role models for the industry.

Did I hear a (52)9er?

By: Dave Kochamba

04/29/2020

This past weekend while social distancing at home I was looking for a comedy to watch. While searching I found Tommy Boy, one of my favorite movies from the 1990s starring Chris Farley and David Spade. While there are many hilarious scenes, one of my favorites that can be written about in a blog article is when Tommy (played by Farley) lies to Richard (played by Spade) at the airport saying he left a message that he was going to miss his flight back to his hometown. Richard then proceeds to needle him about the length of time he needed to complete his undergraduate degree.

Tommy: [gets off the airplane] Richard Hayden!

Richard: Tommy.

Tommy: Where’s my Dad? I thought he was supposed to pick me up at the airport?

Richard: He was at the airport this morning, but you weren’t on the plane.

Tommy: He said he had a surprise for me.

Richard: Maybe. I guess that’s why you should’ve called.

Tommy: I did call, earlier, when… using the phone.

Richard: Earlier? When was that?

Tommy: Er… later… When, when then I, I left a message.

Richard: A message? What number did you call?

Tommy: Two… four.. niner… five, six seven…

Richard: I can’t hear you, you’re trailing off. And did I hear a “niner” in there? Were you calling from a walkie-talkie?

Tommy: No, it was cordless.

Richard: You know what? Don’t. Not here, not now.

Tommy: Did you hear I finally graduated?

Richard: Yeah, and just a shade under a decade too. All right.

Tommy: Hey, you know a lot of people go to college for seven years.

Richard: I know. They’re called doctors

Reading this exchange doesn’t do the scene justice, so I recommend watching the clips below if you haven’t seen the movie:

https://www.youtube.com/watch?v=SWBrM117_II

https://www.youtube.com/watch?v=yKA70sI7Kt0

So at this point you may be asking how this all ties into financial planning. Well, if Tommy did attend college for seven years, hopefully his parents planned ahead for his education expenses and contributed to a 529 early in his childhood. 529 plans have received a large amount of attention over the last few years as the cost of undergraduate education has increased. Parents, grandparents, and friends and family members are looking for ways to save for this potentially significant expense. According to the College Savings Plans Network (CSPN), 529 plan assets grew 16% from the prior year to $319.1 billion as of year-end 2017, while the number of accounts rose 3% to 13.3 million. Like many financial products that have become popular, the number of 529 plans being offered to consumers has risen over time as states and investment management companies are looking to get a piece of the market. When selecting a 529 plan, consumers can open a plan through a broker or an account on their own and invest directly. Direct plans typically are the lower-cost option, as broker-sold 529 plans usually have higher annual costs, including commissions on contributions to the fund that can eat into returns.

With the number of 529 plan options available today, how should you proceed with picking a plan? We recommend reviewing state sponsored 529 plans in your state of residence. Many states (Utah, New York, Georgia, South Carolina, Connecticut and others) offer a state income-tax deduction or income-tax credit on residents’ contributions to their state’s own plans. For instance, contributions by Georgia residents to the Path2College 529 plan are deductible up to $4,000 each year per beneficiary for joint income tax filers, and up to $2,000 each year per beneficiary for all others. Georgia income tax filers also have until July 15, 2020 in order to make contributions that can be deductible for tax year 2019. Tax year 2020 contributions to the Path2College 529 plan are deductible up to $8,000 per year per beneficiary for joint filers and $4,000 per year per beneficiary for all other tax filers in the state of Georgia. Incoming rollovers from other 529 plans do not qualify as contributions eligible for the Georgia state income tax deduction.

It is also important to review a 529 plan’s fees. Some plans charge an annual maintenance fee, asset management fee, and/or administrative fee. These fees vary widely depending on the 529 plan. For instance, the Delaware College Investment Plan managed by Fidelity has fees ranging from .05% to .99% depending on the investments selected. The Hawaii 529 plan, HI529, charges a .55% plan management fee (on top of the underlying fund expenses) and a $20 fee for non-residents according to their program description. TIAA, who manages the Georgia Path2College 529 Plan, recently reduced its program management fee to .07 percent, down from .08 percent, effective last May in recognition of plan assets reaching $3 billion. The plan has no sales charges, enrollment fees, or other maintenance fees, making it among the lowest cost 529 college savings plan in the country.

A great resource in reviewing 529 plans is Morningstar’s annual 529 ratings report. Their 2019 report assigned ratings to 62 plans, which represent more than 97% of assets invested in 529 plans. They named 30 plans as the best of the bunch rating the top plans Gold, Silver, or Bronze. However, five plans received negative ratings from the Morningstar analysis, meaning they have at least one flaw that may make them worth avoiding for most college savers, such as an unstable investment team or high fees.

Now that you have some tips on what to look for in evaluating 529 plans, here’s hoping that the beneficiary of your 529 plan won’t need seven years to complete their degree like Tommy did. And if the beneficiary of your plan does need seven years or more, hopefully they have an M.D. or Ph.D. after their name. If you have any questions related to 529 plans, please contact a member of your Homrich Berg service team.

HB Perspective on Market Expectations and U.S. GDP

04/26/20

We hope our communication this week continues to find you healthy and enjoying quality time with your family. It is hard to believe that it has been six weeks since most of the country entered into this shelter-in-place environment and we all look forward to a gradual return to some level of normalcy over the coming weeks and months. Currently, there is a wide dispersion of opinions in the media on the recovery of the economy and we thought we’d provide you our perspective in this commentary.

Over longer time periods, stocks tend to follow the path of corporate earnings. However, in the short term, they can be driven by a number of factors. These daily, weekly, and monthly moves are heavily influenced by investor expectations. The stock market’s value today is a reflection of, and is pricing in, future expectations, whether positive or negative. We believe short-term moves are often then a consequence of a change in expectations as investors receive more information. For example, if a public company is expected to have a 5% loss in earnings but reports only a 2% loss, the company’s stock will likely increase in value because it beat expectations. The same is true for a company that reports positive earnings of 5%, but comes in below expectations of 7%, its stock price will likely decline in value even though it had positive earnings. The move was determined by what was previously priced into its value already — the expectations.

We’ve seen how expectations have impacted financial markets in the last few weeks. The stock market was near its recent lows in late March when coronavirus deaths dominated the news and the forecasts were dire regarding how far we might be from a peak. Modeling was showing a wide range of scenarios from 100,000 to over 200,000 U.S. deaths. However, in early April updated modeling accounting for the social distancing measures enacted began to show expected U.S. deaths to be significantly lower than first thought, in the range of 60,000-70,000 deaths, and hot spot states such as New York also began to see some improvement. Even the lower projections would have seemed unthinkable to many in January, but given that 60,000 is significantly lower than 200,000 possible deaths, it was a positive change in the outlook. During these same few weeks, the U.S. economy lost over 22 million jobs while the S&P 500 rebounded over 30% at one point off its lows. It’s hard to rationalize how those two could occur at the same time, but it appears the unprecedented job losses were priced in early as the shelter-in-place mandates were enacted.

This week, another important economic indicator will be reported: first quarter’s U.S. GDP growth. This measure is the percentage change in gross domestic product from the previous quarter, annualized. Given the lockdowns were enacted unevenly across the U.S., it’s been hard to estimate how bad this number could be. It is very likely that we could see a large negative number this week, but it may not be quite as bad as it appears. For example, it may be reported that U.S. GDP declined as much as 30%. That does not mean GDP dropped 30% from the fourth quarter. The 30% drop indicates that GDP declined 7.5% from the prior quarter, but that number is then multiplied by four to be annualized which can make for a misleading headline. Current expectations are for a number lower than -30% annualized, but remember no matter what number is announced that it has been annualized.

Looking forward, it is very likely that second quarter GDP reported at the end of July will be even worse, and that the third quarter and fourth quarters will surely be impacted as well. However, it’s likely we will be in some form of a recovery in the second half of this year. We know parts of the economy have been completely shut down and many sectors will continue to be for many months ahead. As we discussed in our last investment email, a ‘V’ recovery is unlikely for jobs or GDP. During the 2008 recession, GDP declined for a total peak-to-trough drop of 4%. Over the course of the Great Depression, by contrast, GDP fell 26%.

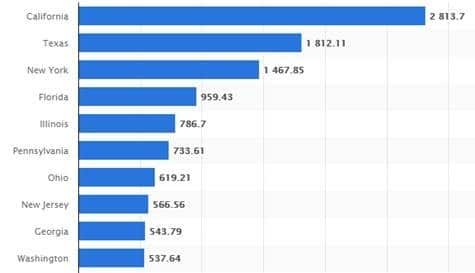

Although the GDP number next week may not be as scary as it first appears, the level of unemployment, the need for more stimulus, and the other economic realities still lead us to believe that the recovery will be quite gradual. Georgia made national headlines this week by beginning to lift restrictions. There are other individual states and groups of states working together that are looking at how to open their economies over the coming weeks. However, for many states reopening is not likely to happen soon. California, which is the fifth largest economy in the world, ranking ahead of India and behind Germany, and New York, the U.S.’s third largest economy, are both not looking at reopening anytime soon. California and New York alone make up about 23% of U.S. GDP. In addition, as the world continues to be locked down the demand for oil has plummeted which has left many oil-related companies facing substantial job losses and even bankruptcy. The entire energy sector is suffering which will should have a prolonged impact on energy-dependent Texas, which is the second largest economy in the U.S.

Ten Largest States by GDP for Q4 2019 (data in millions)

Source: Statista 2020

Just this past week on national television, a small business owner from Decatur was explaining the issues she faced in reopening her business. Requirements for sanitation and use of personal protection equipment (PPE) will not be easily met in the current environment. Select businesses may be able to continue to take advantage of online sales, delivery options, and reopen store fronts quicker. However, many parts of the economy may be more like a turtle’s head coming out of its shell slowly and tentatively, and probably a little jumpy. We imagine many of us, as consumers, will be that way too. Ultimately, widespread testing and viable medical options including a vaccine and/or effective treatments will be needed for the economy to fully open. The government passed another stimulus bill this week to help more small businesses, but additional aid may be needed to support local and state governments as their budgets are hit by lower tax revenues due to the shutdowns.

We certainly hope for the best as we begin to reopen and move towards a recovery, but we acknowledge that we are still dealing with many unknowns. The stock market has rebounded more than expected, and we believe it is currently expecting, or pricing in, a pretty rosy scenario this summer. The risk is if those rosy expectations are not fully met, the stock market may wither back to a reality where the recovery will be a little more gradual and a little tougher. As we expect it won’t be a smooth ride until the recovery is well entrenched, we continue to stay firm believers that a maintaining a diversified approach, staying within your desired level of risk, and looking for opportunities that present themselves during this challenging time are the best approach. As always, we hope you and your family stay safe and well over the coming months. If you have any questions, please reach out to a member of your client service team.

Disclosures: The information reflects Homrich Berg’s views, opinions and analyses as of April 26, 2020. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. The information does not represent legal, tax, accounting or investment advice; recipients should consult their respective advisors regarding such matters. Certain of the information herein is based on third party sources believed to be reliable but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.

How Can I Help Those Impacted By COVID-19?

By: Kelsey Stone

04/20/20

As the world watches the health and economic impact of COVID-19, many are wondering what they can do to help. While there are many ways to assist in the battle against the virus and support those who have been directly impacted, below is a list of charities that are taking donations to help those that have been affected. This list includes charities on the national level, as well as organizations that are local to our headquarters office in Atlanta. This list does not capture all of the charities that are assisting and supporting those directly impacted, but can be used as a guide and starting point for those wanting to donate.

| Feeding America | www.feedingamerica.org | The nation’s largest hunger-relief organization through a network of food banks, pantries and meal programs. |

| First Responders First | https://thriveglobal.com/categories/first-responders-first/ | Providing essential equipment and protective gear to help frontline healthcare workers and their patients. |

| The Giving Kitchen | www.thegivingkitchen.org | Giving Kitchen provides emergency assistance to food service workers through financial support and a network of community resources. |

| Medshare | www.medshare.org | Providing medical supplies and equipment to hospitals in the U.S. and around the world. |

| Piedmont COVID-19 Infrastructure Fund | https://secure3.convio.net/phfou/site/Donation2?df_id=1480&mfc_pref=T&1480.donation=form1 | Goes towards areas of critical need, including drive-thru testing sites, reconfiguring labs for on-site COVID-19 testing, hospital modifications to increase ICU’s and equipment, technology and operating costs. |

| Atlanta Mission | www.atlantamission.org | Atlanta Mission provides emergency shelter, rehab and recovery services, vocational training, services, and transitional housing. We serve more than 1,000 homeless men, women, and children every day. |

| HOPE Atlanta | www.hopeatlanta.org | HOPE Atlanta provides the most comprehensive approach to tackling homelessness in the Atlanta region with housing, outreach, prevention and emergency services. |

Homrich Berg Financial Planning Update

04/19/20

We hope this message continues to find you in good health and enjoying quality time with your family in these unusual times. Our team continues to be laser focused on helping you and your family navigate all aspects of this current environment. To that end, we believe that the current pandemic, and the government response, has created a unique environment for financial planning. Below are a few financial planning items to be aware of during this crisis. Please reach out to your client service team if you would like to discuss how any of the ideas below may apply to your specific situation.

First, a word of warning about Coronavirus related scams. There has been an uptick in the number of scams recently, some playing off COVID-19 fears. Specifically, be on the lookout for the following:

1) Watch for emails claiming to be from the CDC or WHO. Use sites like www.coronavirus.gov and https://www.cdc.gov/coronavirus to get the latest information.

2) Fake websites, products, and virus tests – Ignore online offers for vaccinations, at-home test kits, or products claiming to cure the virus.

3) Real websites with fake products – Amazon, Walmart, and others have third party sellers that may market tainted, damaged, used, expired and otherwise unsafe products that are in high demand because of the coronavirus. Pay attention to who is selling you a product.

4) Fake fundraising — Unfortunately fraudsters use a crisis to raise money for a supposed victim of coronavirus or a charity group claiming to serve these victims. You can use GuideStar or Charity Navigator to vet charities. We plan to have a HUB blog post soon on our website with some suggested charities as a starting point.

Now let’s review some strategies on how you may be able to benefit from the current market downturn and opportunities created in the government response:

1) Mortgage Refinance – We will continue to look for opportunities to see if refinancing your mortgage may be beneficial. As the pandemic spread, interest rates declined and have stayed near historic lows. As rates declined, banks were flooded with refinance inquiries and in many cases were unable to keep up with demand. However, we expect that the opportunity to refinance will be here for a while as we do not expect rates to move much higher quickly given the current economic situation.

2) Roth Conversions – A conversion from a traditional IRA to a Roth IRA when account values are lower can reduce the taxes owed. You may have received a tax deduction when funding the traditional IRA, but if you did then the funds are fully taxable upon withdrawal. A Roth IRA is the opposite; it is funded with after-tax dollars, and withdrawals (including growth) are tax free. A Roth Conversion is a taxable event in the year in which it is done. Because of the different tax treatment, a Roth Conversion may be advantageous for you now with lower account balances due to the market decline. Also, traditional IRAs are subject to Required Minimum Distributions (RMDs) starting at age 72. Roth IRAs don’t have RMDs during your lifetime, so your money can stay in the account and keep growing tax-free. Remember that all RMDs in 2020 have been waived, which could make 2020 an even more attractive time to do a Roth conversion for some investors.

3) Accelerate funding of 529 or IRA (or other tax-deferred accounts) – If you are saving in a tax deferred vehicle for education or retirement on a monthly basis, consider a lump sum to fund the next several months of contributions. By doing this, you will be buying into more equity exposure while the market is down. This would be most beneficial if your account is allocated mostly in equities, and you have several years before the funds are needed.

Disclosures: The information reflects Homrich Berg’s views, opinions and analyses as of April 19, 2020. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. The information does not represent legal, tax, accounting or investment advice; recipients should consult their respective advisors regarding such matters. Certain of the information herein is based on third party sources believed to be reliable but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.

HB Perspective on Fiscal Stimulus and Deficits

04/12/20

These are certainly unprecedented times. Not only have so many had to deal with the tragic loss of family members, but millions have lost their jobs in a matter of weeks, and quarantine and isolation measures continue to be extended across the country. In response, the government has had to react in unprecedented ways as well to limit the health and economic crisis. As this topic comes up often with clients, we’ll discuss in today’s webinar the massive fiscal response of our government and its potential impact on the deficit and economy going forward.

WEEKLY INVESTMENTS UPDATE

Disclosures: The information reflects Homrich Berg’s views, opinions and analyses as of April 12, 2020. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. The information does not represent legal, tax, accounting or investment advice; recipients should consult their respective advisors regarding such matters. Certain of the information herein is based on third party sources believed to be reliable but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.

HB Perspective on Bear Market Rallies

04/05/20

With large market swings almost every day, it’s easy for investors to allow their emotions to get the best of them. On big down days it feels like stocks will only keep going lower, and on the up days investors hope that they have passed the bottom. If the market continues to go lower, their emotions are tested all over again. Even in the worst historical markets, stocks never went down in a straight line. Bear market rallies are periods during a bear market when stocks quickly appreciate in value in the short term, over days and weeks, before heading back down to new lows. I’ll take you through today’s commentary as I discuss bear market rallies and what factors may determine if the recent rally is sustainable.

WEEKLY INVESTMENTS UPDATE

Disclosures: The information reflects Homrich Berg’s views, opinions and analyses as of April 12, 2020. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. The information does not represent legal, tax, accounting or investment advice; recipients should consult their respective advisors regarding such matters. Certain of the information herein is based on third party sources believed to be reliable but which have not been independently verified. Past performance

Important HB Financial Planning Updates

By Todd Hall

Updated on 04/02/2020

The reaction to the spread of the Coronavirus in the market and the economy has been both swift and significant. In response to this, we have seen several important actions from various levels of government and wanted to make sure you are aware of changes that may impact you. The items listed below are based on legislation such as The Families First Coronavirus Response Act (signed into law on March 18), The Coronavirus Aid Relief and Economic Security (CARES) Act (signed into law March 27), and other emergency actions not included in legislation.

NOTE: All information and recommendations below are based on our understanding as of March 31, 2020.

For Individuals

1. The Federal income tax return due date is automatically extended to July 15. Taxpayers can also defer any tax payments that would normally be due on April 15 until July 15 with no interest or penalties. This includes any payments you need to make with your 2019 return, as well as first quarter 2020 estimated payments. No extension form or other paperwork is needed to obtain an extension. Georgia has announced they will mirror the actions taken at the federal level, and most other states have also decided to the same or something similar. Please contact your client service team if you have questions about your specific state.

HB Recommendation: In general, if you expect to get a refund, consider filing your taxes as soon as possible to get your refund sooner. If you will owe additional taxes for 2019, consider delaying until July.

2. Required Minimum Distributions (RMDs) have been waived for retirement accounts. This waiver applies to Traditional IRAs, Inherited IRAs, SEP IRAs, and SIMPLE IRAs, as well as 401(k), 403(b), and Governmental 457(b) plans.

HB Recommendation: Consider delaying any distributions from retirement plans until next year unless one of the following situations applies to you: 1) you need additional cash to cover expenses, 2) you would like to make a Qualified Charitable Distribution, or 3) you would like to convert some of your IRA to a Roth IRA while values are low due to the market downturn.

3. Coronavirus Relief Payments are being sent to taxpayers in the near future. Payments will be $1,200 for individuals and $2,400 for married couples, plus $500 for each child under 17 years old claimed as a dependent. Payments will be phased out beginning at income limits of $75,000 for individual filers and $150,000 for joint filers. While the rebate is technically a 2020 tax credit, the IRS will initially base eligibility on your 2019 income tax return if you have filed it, otherwise they will use your 2018 return.

Importantly, if the amount you receive is less than you are entitled to based on your 2020 income, you can claim the shortfall when you file your 2020 return. On the other hand, if the amount you receive is more than you would be entitled to, no repayment is required.

HB Recommendation if you made less in 2019 than you did in 2018, and the difference would result in a higher relief payment, consider filing your 2019 return as soon as possible. This would be particularly important if your 2018 income would be above the phase out range and 2019 income was below the phaseout range.

Benefits phase out if adjusted gross income (AGI) is over $150,000 for joint filers ($75,000 if single) and totally phase out by $198,000 for joint filers ($99,000 if single). Even if income is over these limits, you may still be eligible to receive $500 per child under 17.

4. Congress waived the 10% penalty on early retirement plan distributions made in 2020. Individuals under the age of 59 ½ who are impacted by the Coronavirus may withdraw up to $100,000 from retirement accounts without the normal penalty that would otherwise apply. Withdrawals can be made from IRAs, employer-sponsored retirement plans, or a combination both. Taxpayers who take these withdrawals will be able to choose whether to recontribute the withdrawn funds within three years of taking the withdrawal, or pay tax on the amount withdrawn (either way, no 10% penalty applies). Taxpayers who choose to pay tax on the amount withdrawn can opt to recognize all the income in 2020, or spread it evenly over three years (2020, 2021, and 2022).

5. Charitable contribution limitations are temporarily relaxed in two ways. Taxpayers who do not itemize deductions will be eligible to donate up to $300 to a qualified charity and have this count as an “above the line” reduction of adjusted gross income. In addition, the 60% of AGI limitation which normally applies to cash donations will be suspended for 2020 for cash contributions (except for donations to private foundations, donor advised funds, and supporting organizations). However, in order for taxpayers to be able to deduct over 50% of AGI in any year (including 2020), gifts will need to be almost entirely made in cash to public charities (excluding Donor Advised Funds). Taxpayers making gifts consisting of a combination of cash, non-cash, and securities are still limited to the old 20%, 30%, and 50% AGI limits.

6. Federal pandemic unemployment compensation of $600 per week is available to unemployed persons in addition to the amount of unemployment benefits they would normally receive from the state (typically about 62% of prior compensation, but not to exceed $380 per week).

For Businesses

7. The Paycheck Protection Program (PPP) enables business with fewer than 500 employees to obtain potentially forgivable loans administered by the Small Business Administration (SBA).

-

- Loans can be up to 2½ times the qualifying payroll costs, capped at $10 million.

- The intent of the PPP is to provide a short-term lending vehicle for employers to help keep their employees in place. Loan forgiveness eligibility will be based on two criteria:

- Funds must be spent on covered expenses during an 8-week period beginning on the loan closing date.

- Forgiveness will be reduced if borrowers lay off employees. The loan forgiveness is tied to number of employees at the end of the 8-week period divided by the number you had before.

- Covered expenses include payroll (includes amounts paid to independent contractors, but excludes any compensation in excess of $100,000) and some benefits (group HC, retirement plan contributions, paid leave) as well as state/local tax on employees and rent.

- Any amount forgiven is not included in taxable income.

- Loans will be administered by 800 existing SBA-certified lenders, including banks, credit unions, and other financial institutions and will carry interest rates of 1.0% over a 2 year period for any amount not forgiven.

HB Recommendation: Any business that might benefit from this program should begin the application process immediately. Going through your existing banking relationships will be most efficient in most cases, especially if you already have an SBA loan. Your bank may have their own website with details on how to apply. You can also get some additional information here: https://www.sba.gov/funding-programs/loans/paycheck-protection-program

8. The Economic Injury Disaster Loans & Emergency Economic Injury Grants (EIDL) is another program to aid businesses with fewer than 500 employees. This programs provides a loan of up to $2 million, locked in for 30 years at 3.75% (2.75% for nonprofits). In addition, most applicants are eligible for a $10,000 grant to be sent to the applicant within three days of applying. The grant will not need to be paid back under any circumstances. Learn more and apply directly here: https://covid19relief.sba.gov/#/

9. The Employee Retention Credit is available for businesses (regardless of size) whose business is partially or fully suspended by orders from a governmental authority due to the Coronavirus, or who has substantial decline in revenue due to the virus.

-

- This is a refundable payroll tax credit of up to 50% of qualified wages (including health insurance premiums) paid after March 12.

- For eligible employers with 100 or fewer full-time employees, all employee wages paid qualify for the credit, whether the employer is open for business, the employees are working from home, or the business is subject to a shutdown order.

- The qualified wages to be taken into account may not exceed $10,000 of compensation, including health benefits, paid to an eligible employee in a calendar quarter.

- There are rules preventing “double dipping” with this credit and other available benefits.

10. Employers can defer payment of payroll taxes. This deferral enables employers (including the self-employed) to delay paying the employer portion of certain payroll taxes through the end of 2020. Half of the employer 6.2% social security tax for 2020 can be deferred to December 31, 2021, and the other half can be deferred to December 31, 2022.

11. Net Operating Loss (NOL) Rules have been relaxed. Previously, the ability of a taxpayer to use the taxpayer’s NOL carryforwards were subject to an annual limitation based on the taxpayer’s taxable-income and could not be carried back to reduce income in a prior tax year and obtain a refund for taxes paid in the earlier period. Legislation signed on March 27, 2020 amends the Code so that an NOL arising in a tax year beginning in 2018, 2019, or 2020 can be carried back five years and used to offset taxable income during that five-year period, producing a refund that would be paid to the taxpayer. The legislation temporarily removes the percentage of taxable income limitation enacted as part of the 2017 Tax Cuts and Jobs Act (TCJA) and allows an NOL to fully offset the taxpayer’s taxable income. Although these changes will allow a more tax-efficient use of NOLs by taxpayers, they will also require that companies amend prior tax returns in order to capture the benefit of the NOL carryback.

12. Recent legislation also provides a technical correction to the 2017 Tax Cuts and Jobs Act (TCJA) for qualified improvement property. Because of an unintended technical glitch in the TCJA, “qualified improvement property” (certain leasehold improvements, restaurant property, and retail property improvements) did not qualify for 100% bonus depreciation. The CARES Act fixes that.

Important HB Financial Planning Updates

03/31/20

The reaction to the spread of the Coronavirus in the market and the economy has been both swift and significant. In response to this, we have seen several important actions from various levels of government and wanted to make sure you are aware of changes that may impact you. The items listed below are based on legislation such as The Families First Coronavirus Response Act (signed into law on March 18), The Coronavirus Aid Relief and Economic Security (CARES) Act (signed into law March 27), and other emergency actions not included in legislation.

NOTE: All information and recommendations below are based on our understanding as of March 31, 2020.

For Individuals

1) The Federal income tax return due date is automatically extended to July 15. Taxpayers can also defer any tax payments that would normally be due on April 15 until July 15 with no interest or penalties. This includes any payments you need to make with your 2019 return, as well as first quarter 2020 estimated payments. No extension form or other paperwork is needed to obtain an extension. Georgia has announced they will mirror the actions taken at the federal level, and most other states have also decided to the same or something similar. Please contact your client service team if you have questions about your specific state.

HB Recommendation: In general, if you expect to get a refund, consider filing your taxes as soon as possible to get your refund sooner. If you will owe additional taxes for 2019, consider delaying until July.

2) Required Minimum Distributions (RMDs) have been waived for retirement accounts. This waiver applies to Traditional IRAs, Inherited IRAs, SEP IRAs, and SIMPLE IRAs, as well as 401(k), 403(b), and Governmental 457(b) plans.

HB Recommendation: Consider delaying any distributions from retirement plans until next year unless one of the following situations applies to you: 1) you need additional cash to cover expenses, 2) you would like to make a Qualified Charitable Distribution, or 3) you would like to convert some of your IRA to a Roth IRA while values are low due to the market downturn.

3) Coronavirus Relief Payments are being sent to taxpayers in the near future. Payments will be $1,200 for individuals and $2,400 for married couples, plus $500 for each child under 17 years old claimed as a dependent. Payments will be phased out beginning at income limits of $75,000 for individual filers and $150,000 for joint filers. While the rebate is technically a 2020 tax credit, the IRS will initially base eligibility on your 2019 income tax return if you have filed it, otherwise they will use your 2018 return.

Importantly, if the amount you receive is less than you are entitled to based on your 2020 income, you can claim the shortfall when you file your 2020 return. On the other hand, if the amount you receive is more than you would be entitled to, no repayment is required.

HB Recommendation if you made less in 2019 than you did in 2018, and the difference would result in a higher relief payment, consider filing your 2019 return as soon as possible. This would be particularly important if your 2018 income would be above the phase out range and 2019 income was below the phaseout range. Benefits phase out if adjusted gross income (AGI) is over $150,000 for joint filers ($75,000 if single) and totally phase out by $198,000 for joint filers ($99,000 if single). Even if income is over these limits, you may still be eligible to receive $500 per child under 17.

4) Congress waived the 10% penalty on early retirement plan distributions made in 2020. Individuals under the age of 59 ½ who are impacted by the Coronavirus may withdraw up to $100,000 from retirement accounts without the normal penalty that would otherwise apply. Withdrawals can be made from IRAs, employer-sponsored retirement plans, or a combination both. Taxpayers who take these withdrawals will be able to choose whether to recontribute the withdrawn funds within three years of taking the withdrawal, or pay tax on the amount withdrawn (either way, no 10% penalty applies). Taxpayers who choose to pay tax on the amount withdrawn can opt to recognize all the income in 2020, or spread it evenly over three years (2020, 2021, and 2022).

5) Charitable contribution limitations are temporarily relaxed in two ways. Taxpayers who do not itemize deductions will be eligible to donate up to $300 to a qualified charity and have this count as an “above the line” reduction of adjusted gross income. In addition, the 60% of AGI limitation which normally applies to cash donations will be suspended for 2020 for cash contributions (except for donations to private foundations, donor advised funds, and supporting organizations). However, in order for taxpayers to be able to deduct over 50% of AGI in any year (including 2020), gifts will need to be almost entirely made in cash to public charities (excluding Donor Advised Funds). Taxpayers making gifts consisting of a combination of cash, non-cash, and securities are still limited to the old 20%, 30%, and 50% AGI limits.

6) Federal pandemic unemployment compensation of $600 per week is available to unemployed persons in addition to the amount of unemployment benefits they would normally receive from the state (typically about 62% of prior compensation, but not to exceed $380 per week).

For Businesses

7) The Paycheck Protection Program (PPP) enables business with fewer than 500 employees to obtain potentially forgivable loans administered by the Small Business Administration (SBA).

- Loans can be up to 2½ times the qualifying payroll costs, capped at $10 million.

- The intent of the PPP is to provide a short-term lending vehicle for employers to help keep their employees in place. Loan forgiveness eligibility will be based on two criteria:

- Funds must be spent on covered expenses during an 8-week period beginning on the loan closing date.

- Forgiveness will be reduced if borrowers lay off employees. The loan forgiveness is tied to number of employees at the end of the 8-week period divided by the number you had before.

- Covered expenses include payroll (includes amounts paid to independent contractors, but excludes any compensation in excess of $100,000) and some benefits (group HC, retirement plan contributions, paid leave) as well as state/local tax on employees and rent.

- Any amount forgiven is not included in taxable income.

- Loans will be administered by 800 existing SBA-certified lenders, including banks, credit unions, and other financial institutions and will carry interest rates of less than 4% (if not forgiven).

HB Recommendation: Any business that might benefit from this program should begin the application process immediately. Going through your existing banking relationships will be most efficient in most cases, especially if you already have an SBA loan. Your bank may have their own website with details on how to apply. You can also get some additional information here: https://www.sba.gov/funding-programs/loans/paycheck-protection-program

8) The Employee Retention Credit is available for businesses (regardless of size) whose business is partially or fully suspended by orders from a governmental authority due to the Coronavirus, or who has substantial decline in revenue due to the virus.

- This is a refundable payroll tax credit of up to 50% of qualified wages (including health insurance premiums) paid after March 12.

- For eligible employers with 100 or fewer full-time employees, all employee wages paid qualify for the credit, whether the employer is open for business, the employees are working from home, or the business is subject to a shutdown order.

- The qualified wages to be taken into account may not exceed $10,000 of compensation, including health benefits, paid to an eligible employee in a calendar quarter.

- There are rules preventing “double dipping” with this credit and other available benefits.

9) Employers can defer payment of payroll taxes. This deferral enables employers (including the self-employed) to delay paying the employer portion of certain payroll taxes through the end of 2020. Half of the employer 6.2% social security tax for 2020 can be deferred to December 31, 2021, and the other half can be deferred to December 31, 2022.

10) Net Operating Loss (NOL) Rules have been relaxed. Previously, the ability of a taxpayer to use the taxpayer’s NOL carryforwards were subject to an annual limitation based on the taxpayer’s taxable-income and could not be carried back to reduce income in a prior tax year and obtain a refund for taxes paid in the earlier period. Legislation signed on March 27, 2020 amends the Code so that an NOL arising in a tax year beginning in 2018, 2019, or 2020 can be carried back five years and used to offset taxable income during that five-year period, producing a refund that would be paid to the taxpayer. The legislation temporarily removes the percentage of taxable income limitation enacted as part of the 2017 Tax Cuts and Jobs Act (TCJA) and allows an NOL to fully offset the taxpayer’s taxable income. Although these changes will allow a more tax-efficient use of NOLs by taxpayers, they will also require that companies amend prior tax returns in order to capture the benefit of the NOL carryback.

11) Recent legislation also provides a technical correction to the 2017 Tax Cuts and Jobs Act (TCJA) for qualified improvement property. Because of an unintended technical glitch in the TCJA, “qualified improvement property” (certain leasehold improvements, restaurant property, and retail property improvements) did not qualify for 100% bonus depreciation. The CARES Act fixes that.

Disclosures: The information reflects Homrich Berg’s views, opinions and analyses as of March 31, 2020. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. The information does not represent legal, tax, accounting or investment advice; recipients should consult their respective advisors regarding such matters. Certain of the information herein is based on third party sources believed to be reliable but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.

HB Perspective on Three Critical Responses to a Financial Crisis

03/29/20

As the $2 trillion coronavirus response bill was a major headline this week, we wanted to give our perspective on the two ways that government can respond in a financial crisis that are critical to its potential depth and length – its monetary and fiscal policies. The Fed drives the monetary policy, while it’s Congress’ job to handle the fiscal response. The Fed tends to act first, as it has in the current crisis. It often takes longer for politics to work themselves out between the House, the Senate, and the White House administration. In this webinar, we’ll discuss what the Fed and Congress have done so far. We’ll also cover how the investor can respond and what we can manage together within your financial plan and investment portfolio. Please note that some of this presentation was recorded right before the final passage of the bill on Friday, but all information is correct and updated. Again, we hope you and your family are doing well and are healthy at this time. If you have any further questions, please reach out to a member of your service team.

WEEKLY INVESTMENTS UPDATE

Disclosures: The information reflects Homrich Berg’s views, opinions and analyses as of March 29, 2020. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. The information does not represent legal, tax, accounting or investment advice; recipients should consult their respective advisors regarding such matters. Certain of the information herein is based on third party sources believed to be reliable but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.

Tips for Families Staying At Home During The Virus Shutdown

By: Todd Hall

03/24/2020

During this time of uncertainty, social distancing, and strange work environments, Homrich Berg would like to share some helpful resources with you and your loved ones. Like many of you, our employees are adjusting to the need to work remotely and, in many cases, to home-school their kids at the same time.

We encourage you to share this blog with anyone who may find it helpful. Please do not hesitate to contact us for anything at this time.

Grocery Delivery and Pick-Up Services:

Publix Grocery Delivery https://delivery.publix.com/

Kroger Grocery Delivery https://www.kroger.com/i/ways-to-shop/delivery

Kroger Grocery Pick-Up https://www.kroger.com/topic/clicklist

Target Pick-Up https://www.target.com/c/order-pickup/-/N-ng0a0

Wal-Mart Grocery Delivery https://grocery.walmart.com/

Amazon Prime Now Grocery Delivery https://primenow.amazon.com/

Costco Grocery Delivery: https://www.costco.com/my-life-costco-grocery-online-delivery.html

Food Delivery Services:

Uber Eats https://www.ubereats.com/

DoorDash https://www.doordash.com/

GrubHub https://www.grubhub.com/

Postmates https://postmates.com/

Official websites to keep up with rapidly evolving efforts to fight the virus and protect the economy

Federal Government multiple agency information site: www.Coronavirus.gov

CDC updates: https://www.cdc.gov/coronavirus/2019-ncov/index.html

IRS updates: https://www.irs.gov/coronavirus

State of Georgia COVID-19 Webpage: https://dph.georgia.gov/novelcoronavirus

Tips for Working at Home:

https://www.npr.org/2020/03/15/815549926/8-tips-to-make-working-from-home-work-for-you

https://www.businessinsider.com/how-to-work-from-home-during-the-coronavirus-outbreak-2020-3

https://www.cbsnews.com/news/coronavirus-pandemic-tips-for-working-from-home/

Ideas and Free Educational Materials for Kids at Home:

- Crash Course YouTube Channel – Online courses on various subjects from Astronomy to US History and Anatomy & Physiology

- Crash Course Kids Youtube Channel – This bi-weekly show from the producers of Crash Course is all about gradeschool science.

- Smarter Every Day YouTube Channel – An entertaining channel dedicated to exploring the world using science.

- Scholastic Learn at Home— Daily projects for kids in pre-K through grade 9.

- Epic— A digital library for kids up to age 12.

- Khan Academy— Short online courses in subjects ranging from world history to economics, along with sample daily schedules to help get kids on a routine.

- Outschool— Live online classes for kids ages 3 to 18.

- BrainPop— Lessons in all subjects for kindergarten through grade 8; some school districts are supplying parents with passwords to log in free of charge.

- Org— Online coding classes.

Things are changing rapidly on all fronts. If you liked this post please feel free to sign up for future blog updates here.

If you have questions don’t hesitate to reach out to your HB team. If you do not have an HB service team, click here to contact us or click here to learn more about Homrich Berg.

A Message From Andy Berg

03/22/20

While the markets and all of us take a deep breath after another week full of constant news updates and market swings, I wanted to take a moment to offer a few personal thoughts to you. First, I hope and pray you and your families are healthy. We are all hopeful that progress continues on treatments for this virus and that our healthcare system successfully treats all who are sick in the weeks ahead.

We have been working day and night across our entire firm to monitor the markets, develop and implement our investments and planning recommendations, and communicate with you often as the situation continues to evolve. Our investment committee is meeting daily via conference call and our entire firm is “all hands on deck” to serve you. Investments that we made in software and technology in order to be able to operate remotely are obviously needed now and proving to be very successful. We have sent out multiple emails to you to keep you updated on our views, and will continue to do so. We are gathering common questions from our client service teams and will cover those in a future communication. As always, we encourage you to reach out to me or your team if you have any concerns or questions that you would like addressed.

As I said in a recent audio message to clients, I have seen many crisis moments in the markets during my career. Every time the reasons are different, and every time it is hard for some investors to stay calm in the middle of the chaos. This is the time where we shine as advisors, both because we have built a financial plan with you that has an allocation that should be able to weather tough times, and because we are here for you to advise you and keep you on track during the intensity of the unsettling news and big market moves. Also, these kinds of crisis moments can be some of the best times to buy stocks, and this is why we sent our recent communication about our client trading activity including rebalancing back to your stock targets, harvesting tax losses, and setting targets for future additions to stocks if prices keep getting cheaper. Our role as your advisor is to stay calm and keep focused on the opportunities.

There will likely be more tough days in the markets, but I remain consistently optimistic that we will recover and thrive on the other side of this virus battle. We will continue to work hard for you and look forward to brighter days ahead.

Disclosures: The information reflects Homrich Berg’s views, opinions and analyses as of March 22, 2020. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. The information does not represent legal, tax, accounting or investment advice; recipients should consult their respective advisors regarding such matters. Certain of the information herein is based on third party sources believed to be reliable but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.

- « Previous Page

- 1

- …

- 12

- 13

- 14

- 15

- 16

- …

- 23

- Next Page »