05/11/20

As a majority of states have now begun a phased reopening, we continue to hope that you and your family are well and healthy. We often hear about the differences between Wall Street and Main Street when it comes to the economy. Wall Street represents the financial markets and big business. Main Street is represented by small businesses, individuals, and the economy at the local level. During the pandemic, the contrast between the two economies has become quite evident. Even though over 30 million Americans have filed for unemployment, the S&P 500 is only down 10.3% year to date as of May 7. Wall Street and Main Street appear to have two different views of the economy, and likely their respective paths to recovery will be different as well. National attention was drawn to this contrast, recently, when some public companies made headlines as they were able to access Paycheck Protection Program loans first while many small businesses were left waiting in line when the initial funding ran out.

As mentioned, the Wall Street economy is that of larger firms, which have outperformed their smaller peers in the stock market this year. The theme – that bigger is better and biggest is best – is becoming more apparent in the stock market and economic recovery. Larger firms simply have more resources and levers to pull to sustain themselves through recent events and many are striving to gain market share through the pandemic. While the corner pizzeria, dentist or local hardware store has had to close up or has limited ability to serve customers, companies such as Amazon have had historic demand for their products and deliveries, which is reflected in their stock price.

This is even evident within the large company universe, itself. As of May 4, the top five stock weightings in the S&P 500 were Microsoft (5.2%), Apple (4.9%), Amazon (3.4%), Google (3.2%) and Facebook (1.9%). Although Apple, Google and Facebook are slightly positive at 3.7%, 3.4% and 2.9%, respectively, they are outperforming the broader market considerably, and Microsoft is up 16.7% while Amazon is up 28.1%. In fact, a cap-weighted portfolio of these top five companies is outperforming the S&P 500 by 21.8%. It’s up 11.5%, while the S&P 500 is down 10.3%.

We also see this trend with other top firms in their sectors including Walmart, Adobe, Netflix, and Home Depot as just a few examples which were up 3.5%, 11.2%, 34.9%, and 5.8% year to date, respectively. Even though the entire retail sector has been hit hard, larger companies are generally outperforming their smaller peers. As of May 4, there were 40 companies that had year-to-date returns above 10%. However, there were 331 companies that had stock prices down more than 10%, including 197 companies that were down more than 25%. Those large companies we singled out are real outliers.

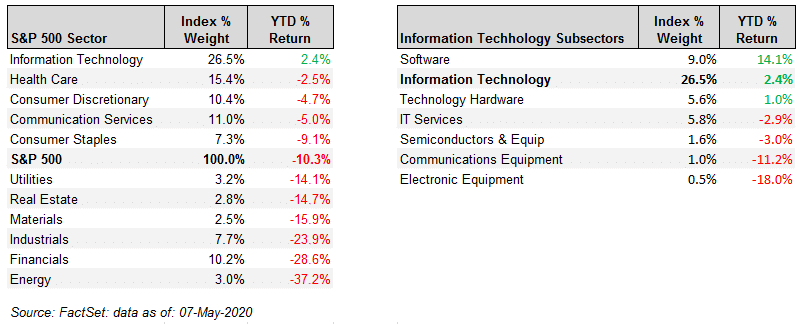

The chart below on the left shows that Technology is the largest weighting and the best performing sector in 2020. Healthcare, the second largest weighting and the second-best performer, is also comprised of large companies that have scale and staying power.

The chart on the right shows the subsectors in Technology and how the returns have been driven by a few companies within the Software sector which include of course Microsoft, but also Oracle, Intuit, Citrix, Salesforce, to name a few large ones that have also outperformed the broader market during the pandemic. To be sure, the recent challenges seem to be accelerating some broad economic trends that were already underway—particularly in retail, entertainment and technology.

We believe the different economic realities between Wall Street and Main Street may exist for some time, and even as the economy gradually recovers. This phenomenon reminds us of the need to try to capitalize on these Wall Street advantages in a diversified investment plan to benefit our clients on Main Street. That plan is customized to fit each client’s unique situation, goals and risk tolerance. If you have any further questions on this topic, please contact a member of your service team.

Disclosures: The information reflects Homrich Berg’s views, opinions and analyses as of May 10, 2020. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. The information does not represent legal, tax, accounting or investment advice; recipients should consult their respective advisors regarding such matters. Certain of the information herein is based on third party sources believed to be reliable but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.