05/06/2020

First and foremost, we hope you and your family are safe and well during this health crisis. After seven weeks of successfully working from home, we are making plans to reopen our offices. We plan to share details of our plan later this week.

In our continued effort to communicate through these challenging times, we want to focus today upon recent developments in the bond market. Although stock market movements tend to dominate headlines, the bond market is actually quite larger in size and represents an important allocation for nearly every investor. Debt is really what keeps the engine of corporate America running smoothly and when there are disruptions, as we have recently observed during the pandemic, it has wider implications for the financial system.

In the bond market, Treasuries are considered a “safer” investment as they are backed by the full faith and credit of the U.S. government, and therefore Treasuries typically feature lower yields (interest rates). When there is turmoil brewing in the economy, investors tend to sell riskier investments and buy Treasuries as a “safe-haven” investment. Like the stock market, the bond market is comprised of many sectors and each features unique risks and return trade-offs. Examples include: Treasuries, mortgage-backed securities, municipal, investment grade corporate, asset-backed securities, high-yield (junk bonds), and emerging market debt, among others. The level of perceived risk in a given category is measured by its “spread”. The spread is the difference between a bond yield of a given maturity, credit rating, issuer, or risk level as compared to a similar Treasury bond—the higher the perceived risk, the higher the spread.

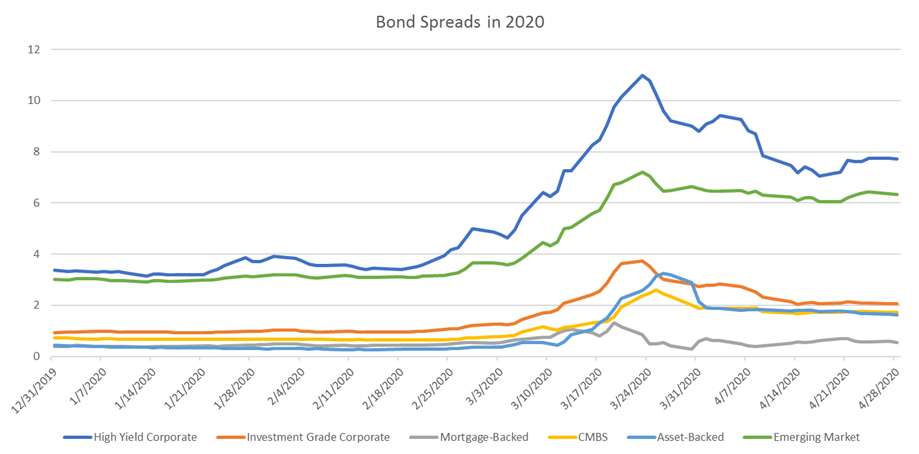

During periods of economic stress, spreads can increase significantly as the value of riskier bonds decrease causing yields to rise. As the economic damage began to unfold in March, spreads widened dramatically across many sectors including those shown in the chart below. Redemptions from mutual funds and margin calls for hedge funds and mortgage REITs created an environment with the forced-selling of bonds in order to raise cash with very few buyers.

Although stock market volatility dominated headlines, the volatility and illiquidity in the bond market may have been more surprising and—in some cases—was just as severe. We can see that High Yield and Emerging Market debt had a higher spread to begin the year to reflect their riskier nature, but those spreads increased even more than the typically safer sectors of investment grade corporate, mortgage-backed, and asset-backed bonds over the rest of the month. Spreads increased through much of March as there continued to be more sellers than buyers until the Fed began to purchase bonds in late March. The Fed began with $700 billion in bond purchases, and it then followed with an unlimited and open-ended plan to purchase corporate and municipal bonds. This was later revised to encompass some high yield bonds in April. The Fed was willing to buy almost anything just short of equities. Their goal was to keep financial systems functioning, intact, and able to extend credit both through the crisis and also after the recovery begins. Its goal was largely achieved as markets began to settle down in early April.

Given the Fed’s action to cut interest rates to practically zero and the slower expected economic growth, it is likely that yields will remain low for an extended period. Still, we believe bonds remain an essential part of a diversified portfolio for liquidity and capital preservation. During the early moments of this crisis we reduced bond risk and focused on cash and Treasury backed money-market funds to allow time for the liquidity crisis to pass, but we have now moved back into ultra-short duration bond funds and traditional money market funds to improve yield income while keeping interest rate risk lower. In times of low rates we will continue to emphasize shorter maturity bonds to reduce the risk of future yield increases that may hurt bonds down the road. We do not believe investors are getting paid enough extra yield to go into longer maturities today. Even though we believe yields will likely remain less attractive for some time, it is our view that there are sectors of the bond market where there are still good fundamentals such as mortgage- or asset-backed bonds that can provide a higher yield and price appreciation opportunities. We will continue to look for investment opportunities within the bond markets while also continuing to recognize the liquidity and capital preservation role they play in client portfolios. If you would like to discuss further please contact a member of your service team.

Disclosures: The information reflects Homrich Berg’s views, opinions and analyses as of May 3, 2020. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. The information does not represent legal, tax, accounting or investment advice; recipients should consult their respective advisors regarding such matters. Certain of the information herein is based on third party sources believed to be reliable but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.